Identity Fraud vs Identity Theft: Which Requires Police Reports and Credit Freezes:

Identity theft involves someone stealing your personal information. Identity fraud involves someone using that stolen information for financial gain. Identity theft often triggers a credit freeze. Identity fraud usually requires bank disputes. Many cases involve both, and understanding which you are dealing with determines what you need to do next.

Someone used your Social Security number to open a credit card you never applied for. Or your bank flagged a loan application you did not submit. Or you found out your personal information was exposed in a data breach and now you are not sure what to do about it.

These situations are not all the same. And the steps you take depend on which one you are actually facing.

The difference between identity fraud vs. identity theft is not just legal hair-splitting. It changes whether you need a police report, a credit freeze, a bank dispute, or all three. This guide breaks it down clearly so you know exactly what you are dealing with and what to do next.

Identity theft is the stealing of your personal information

Identity fraud is the use of that stolen identity for financial gain

Identity theft often requires a credit freeze and police report

Identity fraud usually requires bank disputes and fraud documentation

Many cases involve both, and each step builds on the other

Identity Fraud vs Identity Theft: Key Differences

People use these terms interchangeably, but they describe two different stages of the same crime. Understanding which stage you are in changes the actions you need to take.

Category

Identity Theft

Identity Fraud

Definition

Stealing your personal information

Using stolen identity for financial gain

Financial loss

Not always immediate

Almost always

Credit impact

Possible

Common

Police report

Often recommended

Sometimes required

Credit freeze

Often required

Sometimes required

The simplest way to think about it: identity theft is the break-in. Identity fraud is what happens after. A thief can steal your credentials and sit on them for months before using them. That means you could be a victim of identity theft without knowing it, until the fraud starts.

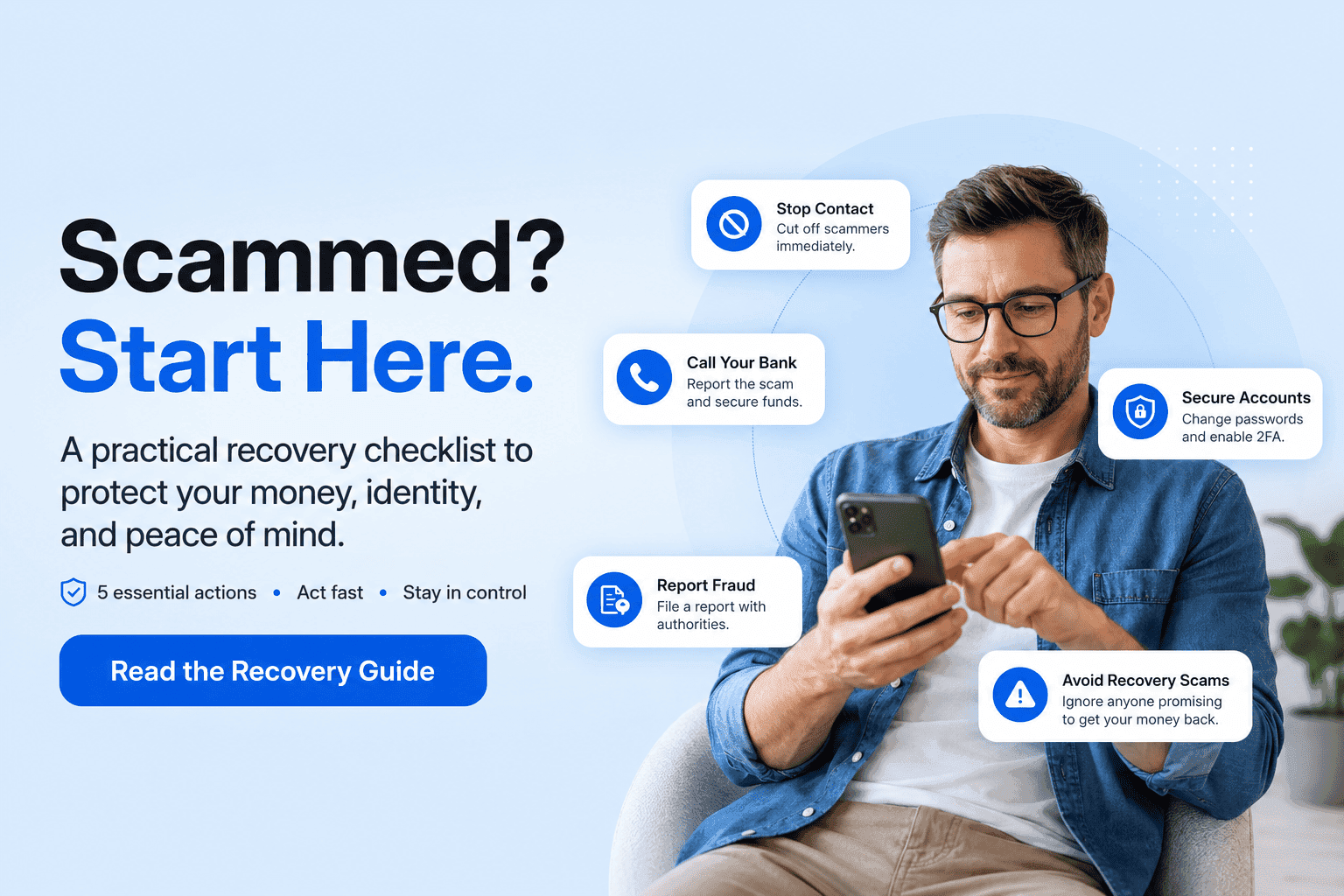

First, build your case with Unscammed to see if you're dealing with identity theft, fraud, or both before contacting the police or your bank.

What Is Identity Theft?

Identity theft is when someone obtains your personal information without your consent. The theft itself may not cause immediate financial damage, but it puts you at serious risk. Your Social Security number, date of birth, address, login credentials, or financial account details can all be stolen and held until the scammer is ready to use them.

Common ways identity theft happens: data breaches at companies that hold your information, phishing attacks that trick you into handing over credentials, physical theft of documents like your wallet or mail, and account takeover through compromised passwords.

Identity Theft Example

Description

Stolen Social Security number

Your SSN is obtained through a breach or scam and can be used to file taxes, apply for loans, or open accounts

Data breach

A company holding your personal data is hacked and your credentials are exposed

Account takeover

A scammer gains access to your existing accounts using stolen login information

Impersonation

Someone uses your identity to establish a fake profile or pass verification checks

If your personal information was exposed but has not been misused yet, you are at the theft stage. This is the moment to act before it becomes fraud.

What Is Identity Fraud?

Identity fraud is what happens when stolen personal information gets used. A criminal opens a credit card in your name, applies for a loan you did not request, files a tax return using your Social Security number, or drains a bank account. This is where the financial damage actually happens.

The distinction matters legally. Identity theft is the crime of obtaining your information unlawfully. Identity fraud is the crime of using it. In practice, both often happen together, but not always at the same time or by the same person.

Identity Fraud Example

Description

Credit card fraud

Unauthorized charges made on existing accounts or new accounts opened in your name

Loan fraud

Fraudulent loan applications submitted using your identity

Bank fraud

Unauthorized withdrawals or transfers from your accounts

Tax fraud

A fake tax return filed under your Social Security number to claim your refund

Both are serious. The better question is which causes more immediate harm, and the answer depends on how far the crime has progressed.

Factor

Identity Theft

Identity Fraud

Immediate financial loss

Rarely

Almost always

Long-term credit impact

Yes

Yes

Recovery time

Can be long

Medium to long

Legal risk and complexity

High

High

Here is what makes identity theft particularly damaging in the long run: you may not know it happened until months or years later, when the fraud is already extensive. A single data breach can expose your credentials to dozens of scammers who sell and trade that information over time.

Identity fraud is more immediately painful because the financial loss is real and visible. But identity theft creates a vulnerability that can be exploited repeatedly.

Many cases involve both. Your information is stolen first. Then it is used. Then it is sold and used again. That is why acting early, before fraud occurs, is so important.

When You Need a Police Report

Not every case of identity fraud vs. identity theft requires a police report, but many do. And having one significantly strengthens your position when disputing with banks and credit bureaus.

Scenario

Police Report Needed

New accounts opened in your name

Yes

Loan fraud using your identity

Yes

Tax return filed under your SSN

Yes

Bank account fraud or unauthorized withdrawals

Sometimes

Identity exposure from data breach only

Not always, but recommended

File a police report when there is documented financial harm or when your bank, credit bureau, or another institution asks for formal supporting documentation. If you have already completed an FTC identity theft report, bring that affidavit with you, along with your timeline, account records, and any proof of fraudulent activity. Many departments will ask for clear supporting evidence when you file.

A police report creates a case number. That case number is what financial institutions and credit bureaus use to verify your claim is legitimate, not just a dispute filed out of frustration.

When to Place a Credit Freeze

A credit freeze stops new creditors from accessing your credit file. This is one of the most effective steps you can take after identity theft, because it prevents a scammer from opening new accounts in your name even if they have your full personal information.

Scenario

Credit Freeze Recommended

Social Security number stolen or exposed

Yes

Personal data exposed in a data breach

Yes

Fraudulent accounts already opened

Yes

Single unauthorized bank transaction

Sometimes

Phishing attack where credentials were entered

Yes

A credit freeze is free. You place it separately with each of the three major credit bureaus: Equifax, Experian, and TransUnion. It does not affect your existing accounts or your credit score. It only stops new credit applications from being processed while the freeze is active.

If you need to apply for credit yourself, you can temporarily lift the freeze and reinstate it afterward.

Can Identity Theft Happen Without Fraud?

Yes. And this is one of the most important things to understand about identity fraud vs identity theft.

Your personal information can be stolen and sit unused for months. A scammer who obtained your Social Security number in a data breach may not use it immediately. They may sell it. The buyer may sit on it. By the time fraud actually occurs, it can be years after the original theft.

This is why monitoring matters even when nothing has gone wrong yet.

Situation

Recommended Action

Data breach notification received

Monitor your credit report closely and consider a freeze

Lost wallet or stolen physical documents

Freeze your credit immediately and place a fraud alert

Phishing email clicked or credentials entered

Change passwords, monitor accounts, and set up alerts

SSN exposed but no fraudulent accounts yet

Place a fraud alert with credit bureaus and file an FTC report

If you know your information was stolen, treat it as a serious threat even if nothing has happened yet. The time between theft and fraud is the window where a credit freeze or fraud alert can stop the damage before it starts.

How to Report Identity Fraud vs Identity Theft

The reporting steps differ depending on whether you are dealing with theft, fraud, or both. In many cases, you will end up doing several of these steps. Start by organizing your evidence, then move into the FTC, your bank, the credit bureaus, and law enforcement based on the type of case you are facing.

For identity theft: File with the FTC first. Place a fraud alert or credit freeze with all three credit bureaus. File a police report if accounts were opened or if you need documentation for disputes. Monitor your credit report closely.

For identity fraud: Contact your bank or creditor immediately to dispute unauthorized transactions. File with the FTC. Provide documentation including transaction records, communication logs, and a police report if required. Request written confirmation of all disputes.

Start with Unscammed to organize your evidence before you contact any institution, so each report you file is based on a cleaner, more complete record of what happened.

Identity Theft vs Impersonation

Impersonation is a specific type of identity misuse that often overlaps with both identity theft and identity fraud. It is worth understanding on its own because it shows up in scams differently.

Impersonation happens when someone pretends to be you, not necessarily by using your credentials, but by adopting your identity in communications, applications, or interactions. A scammer might use your name and Social Security number to apply for government benefits. Or they might use stolen documents to pass identity checks.

Type

Description

Impersonation

Pretending to be the victim in communications or applications

Identity theft

Stealing personal data including SSN, credentials, or documents

Identity fraud

Using stolen identity to commit financial crimes

The lines between these often blur in real cases. A scammer impersonates you by using your stolen identity to commit fraud. All three concepts can apply to the same criminal act. What matters is documenting what happened clearly so that each institution you report to understands the full picture.

How to Protect Against Identity Fraud and Theft

The best time to act is before the fraud happens. Once your information is out there, protection becomes harder. These steps reduce your risk and improve your ability to catch problems early.

Credit Monitoring

Sign up for a credit monitoring service that alerts you when new accounts are opened, inquiries are made, or your personal information appears somewhere unexpected. Many banks offer this free through their apps.

Fraud Alerts

A fraud alert tells lenders to take extra steps to verify your identity before opening new accounts. It is less restrictive than a credit freeze but adds a layer of protection. Place one with any of the three credit bureaus and they are required to notify the other two.

Credit Freeze

The strongest available protection. A freeze blocks all new credit inquiries until you lift it. Free, effective, and available to anyone regardless of whether fraud has occurred yet.

Account Alerts

Set up real-time transaction alerts on every bank account, credit card, and financial account you hold. The faster you spot an unauthorized transaction, the faster you can dispute it.

Protection Method

Key Benefit

Credit freeze

Prevents new accounts from being opened in your name

Fraud alert

Notifies lenders to verify identity before approving credit

Credit monitoring

Detects changes to your credit report in real time

The difference between identity fraud vs identity theft is not just a terminology question. It determines which institutions you contact, what documentation you need, and whether a police report or credit freeze should be your first move.

Identity theft happened to you. Identity fraud is what the criminal did with what they took. In many cases you are dealing with both, and the steps overlap. But knowing which stage you are at helps you prioritize.

If your information was stolen: freeze your credit, file an FTC report, place a fraud alert, and monitor closely.

If fraud has already occurred: dispute with your bank, file a police report, submit your FTC affidavit, and escalate to the CFPB if your claim is denied.

Either way, start by getting your evidence organized. Unscammed helps you document everything clearly before you contact the police, your bank, or the credit bureaus, so you can move faster and support your case more effectively.

FAQ: Identity Fraud vs Identity Theft

Is identity theft the same as identity fraud?

No. Identity theft is the crime of stealing your personal information. Identity fraud is the crime of using that stolen information for financial gain. They often happen together but are legally and practically distinct.

Which is worse: identity fraud or identity theft?

Both are serious. Identity fraud causes immediate financial harm. Identity theft creates a long-term vulnerability that can be exploited repeatedly over time, sometimes without your knowledge for months or years.

How do I report identity fraud?

Contact your bank's fraud department to dispute unauthorized transactions. File a report with the FTC at IdentityTheft.gov. File a police report if new accounts were opened or if your bank requires documentation. Submit to the CFPB if your bank denies your claim.

How do I report identity theft?

File with the FTC at IdentityTheft.gov to generate an official affidavit. Place a fraud alert or credit freeze with all three credit bureaus. File a police report if accounts were opened in your name. Monitor your credit report for new activity.

Can identity theft happen without fraud?

Yes. Your personal information can be stolen and not used immediately. Scammers often sell stolen credentials, meaning fraud can occur months or years after the original theft. This is why acting quickly after a data breach or suspected theft matters.

What counts as identity fraud?

Any use of your stolen personal information for financial gain. This includes opening credit cards or loans in your name, filing a fraudulent tax return, making unauthorized withdrawals from your bank account, or using your identity to pass verification checks for benefits or services.

Being scammed is disorienting, and it can happen to anyone, including careful, smart people who do everything right most of the time. If your stomach just dropped, take that as your cue to act, not to freeze.

Family identity theft is not just one person's credit card being stolen. In a single household you might have children with unused Social Security numbers, elderly parents targeted by phone scams, adults exposed in data breaches, and shared devices or accounts that create extra risk. Each person faces a different threat, and protecting the family means covering all of them.

Share:

Share: