Capital One Fraud Reporting: How to Report Scams, Dispute Charges and Recover Money:

You spotted a charge you didn't make. Or a text popped up about a "suspicious purchase at Foot Locker." Or someone called, sounding very official and calm, and now your stomach is doing that thing where you're not sure what you just agreed to.

Share:

Take a breath. You’re not the first person this has happened to, and you won’t be the last. Scammers targeting Capital One customers have gotten genuinely good. People lost thousands in a single afternoon to a caller who claimed to be from the Capital One fraud department. The script scammers used tends to sound exactly like a real bank employee.

What you do in the next few hours matters more than what you wish you had done yesterday.

The right step depends on what actually happened. An unauthorized charge, a stolen debit card, a billing dispute with a merchant, a phishing link, full-blown identity theft, or a scam where you were tricked into sending money yourself all require different actions. Each scenario has a completely different escalation path at Capital One, and walking through the wrong door just slows down your recovery.

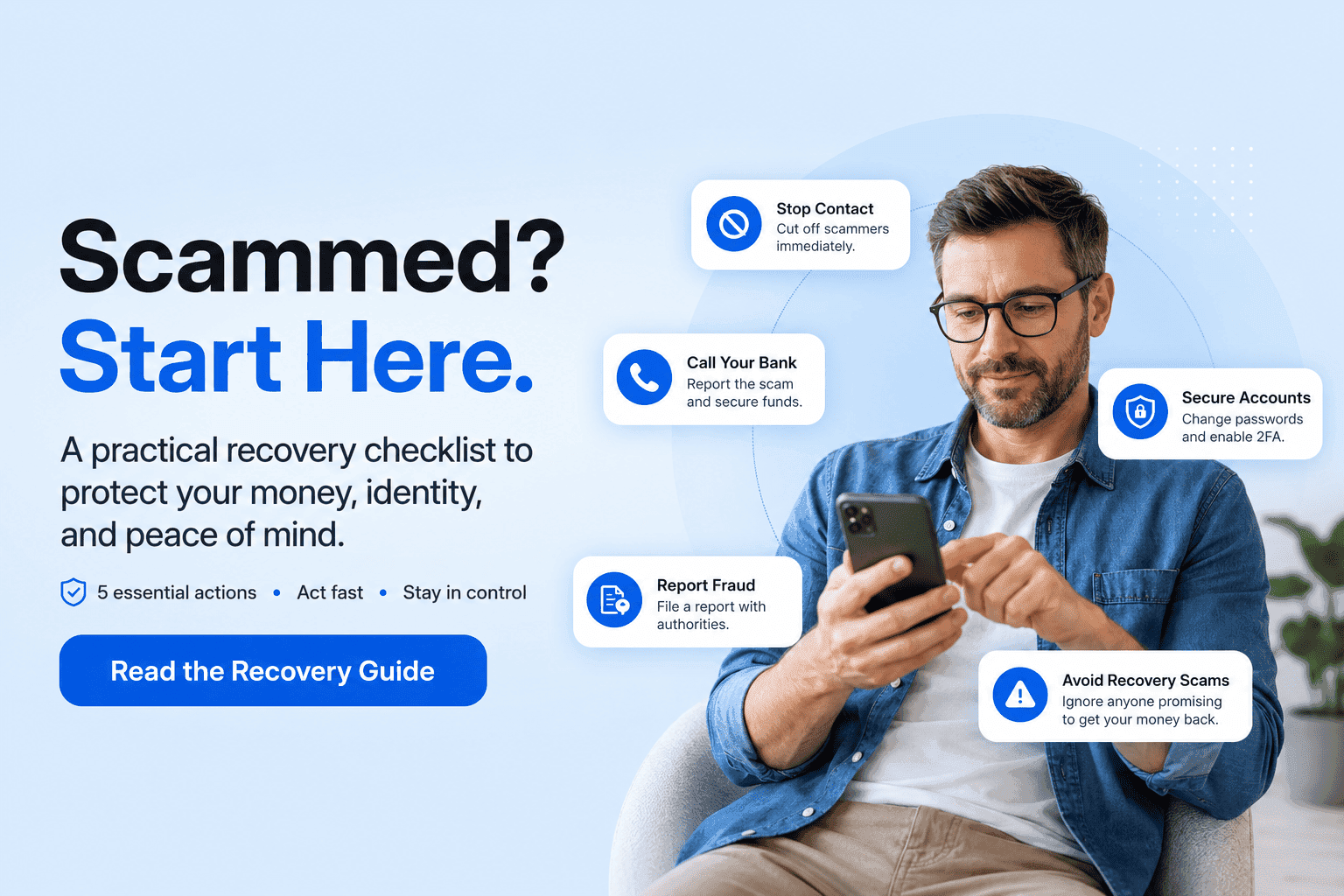

If you’re reading this in panic mode, here’s the short version. Do these things now, in this order. The rest of the article explains each one in detail.

Stop communicating with the scammer.

Don’t click any more links. Don’t share another code, even if they say it’s to cancel something.

Lock the affected card in the Capital One app if you can.

Screenshot everything: the charge, the text, the email, the website URL, the caller ID, the time stamp.

Report the issue through the official Capital One app, website, or phone number on the back of your card.

Change your Capital One password and your email password if your login details may be exposed.

Turn on every stronger security control Capital One offers.

Monitor your credit and bank accounts closely for the next several weeks.

Capital One Fraud Department Phone Number and Live Hours

Capital One doesn’t run a single universal “fraud department” hotline. The channel depends on the product involved. Here’s the cleanest way to see it:

Situation

Official Capital One option

Credit card fraud or suspicious card activity

Use the app/website transaction flow or call the number on the back of your card

Debit card fraud

Call 1-888-464-0727

Scam or compromise concern

Call 1-800-227-4825

Outside the U.S. for scam or compromise concern

Call collect at 1-804-934-2001

General customer service routing

1-877-383-4802

For Capital One credit card fraud

Capital One says you can start a credit card fraud claim directly in the app or on the website. Open recent transactions, select the charge in question, choose Report a problem, and answer the questions about whether you recognize it.

For Capital One debit card fraud

Capital One says debit card fraud should be reported immediately by calling 1-888-464-0727. The transaction usually needs to be posted before a claim can be initiated, but you should still call right away if a pending charge looks wrong and you suspect someone has access to your account or debit details.

For scam or account compromise concerns

Capital One’s scam education page directs customers to call 1-800-227-4825 if they’ve spotted a scam or believe they’ve been compromised. The same page recommends submitting a suspicious activity form and reporting the scam to the FTC and the FBI.

A serious warning

One of the most common Capital One scams in circulation right now works by hijacking what you think is a callback. A victim recently described calling back what looked like a Capital One number and hearing a recording that said, “Thank you for calling Capital One. You’ve reached the fraud department,” before being dumped into a single-option voicemail tree. It sounded real. It wasn’t.

Do not trust phone numbers from search ads, pop-ups, social media comments, text messages, voicemails, or anyone who called you first. Scammers buy lookalike numbers and record fake bank greetings to make their setups feel authentic. Pull out your physical card and dial the number printed on the back. That number is the one number you can be sure of.

Capital One Fraud Claim vs. Dispute: What’s the Difference?

This distinction trips up almost everyone, and it’s the difference between a fast resolution and a stalled case. Capital One treats them as separate processes.

Issue type

What it usually means

Capital One path

Fraud claim

You did not authorize the transaction

Report as fraud

Merchant dispute

You authorized the transaction, but something went wrong

File a dispute

Scam payment

You were tricked into authorizing the payment or sharing info

Report scam/fraud and ask what options apply

Identity theft

Someone used your personal information to open accounts

Report to Capital One and to official identity theft channels

Phishing attempt

Fake Capital One message, call, or site

Report suspicious activity and secure your accounts

Capital One handles disputes and fraud through completely different channels. A dispute applies when you authorized the charge but something went wrong with the transaction, such as a missing delivery, a broken item, a double charge, or a service that failed to match what was promised. A fraud claim applies only when someone uses your account completely without your permission.

The trickiest situations sit right in the middle. If a scammer convinced you to approve a transaction yourself, such as walking you through an app payment for a fake fee disguised as a hotel reservation, banks often do not classify it as unauthorized. You still need to report it immediately, but you must be precise on the phone about how the transaction happened so the representative opens the correct type of case.

Step-by-Step Capital One Dispute Process for Fraudulent or Scam-Related Charges

Step 1: Confirm the charge is posted

Capital One says pending transactions can’t be disputed because the amount may change or drop off entirely. A charge generally posts within about five days. Watch your account, and when it lands, you can move.

Step 2: Check whether this is fraud or a merchant dispute

Before you file, ask yourself:

Did you make or authorize the charge?

Did an authorized user on your account make it?

Is the merchant name unfamiliar but possibly legitimate (the legal business name often differs from the storefront name)?

Is this a forgotten subscription or a free trial that converted?

Was the card lost or stolen?

Has your account been compromised?

Were you tricked into sharing your login, code, or card details?

Capital One specifically recommends checking authorized users, subscriptions, and unfamiliar merchant names before opening a fraud claim. A surprising number of “unrecognized” charges turn out to be a streaming service renewing under its parent company’s name, or a partner’s purchase the cardholder forgot about.

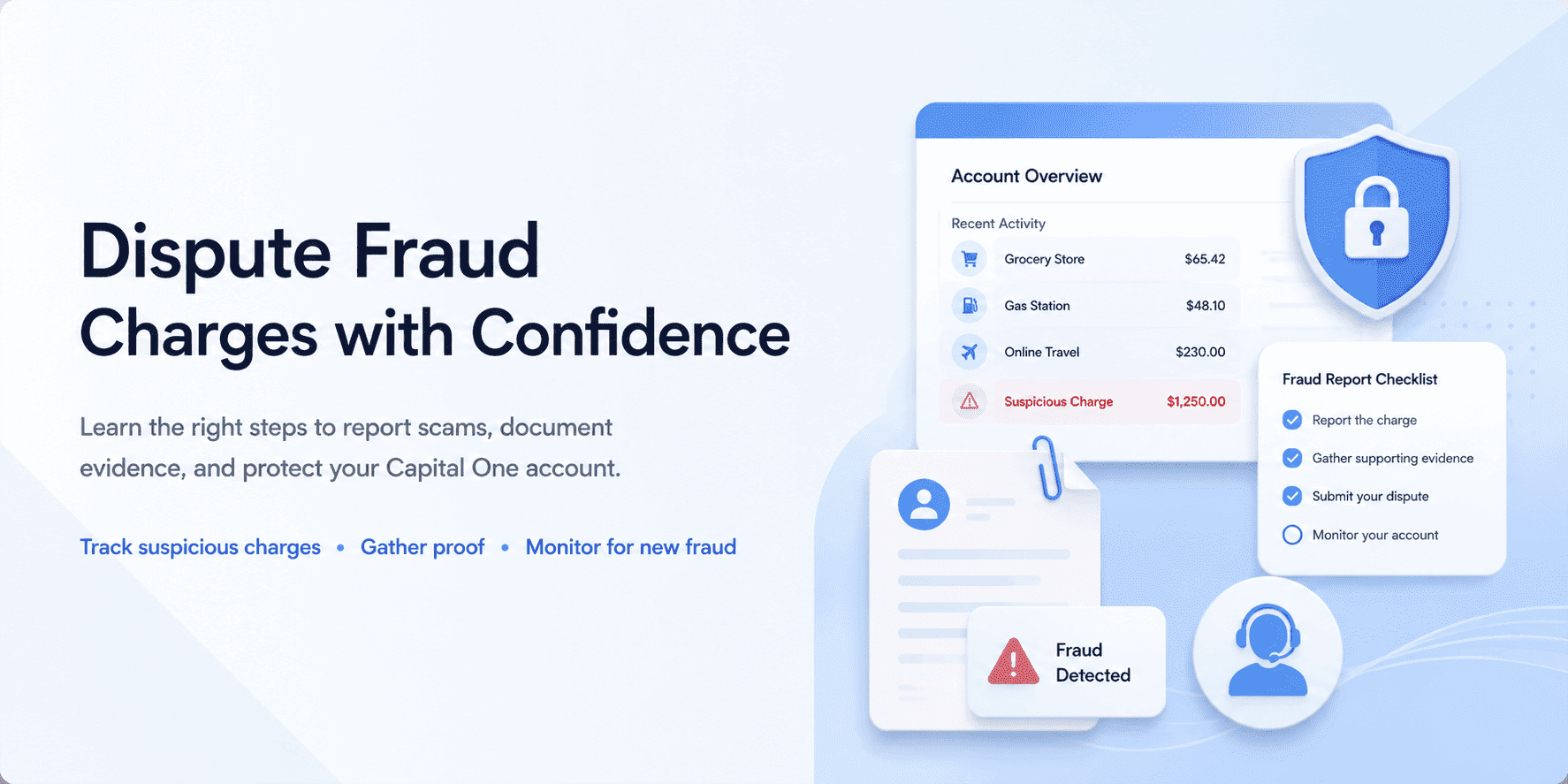

Step 3: Gather your evidence

Pull everything together before you file. Once you start a case, you want to be able to answer every question without scrambling. Read the next section for more information about gathering evidence.

Step 4: File through the Capital One app or website

For credit card issues, open recent transactions, tap the charge, choose Report a problem, and follow the prompts. Capital One says digital disputes generally need to be filed within 90 days of the transaction date. If more time has passed, you can still call the number on the back of the card.

Step 5: Watch for messages and document requests

Capital One may send updates online or by mail. Respond quickly. Keep every case number. If they ask for more documentation, send it the same day if you can.

Step 6: Appeal if the claim is denied

Capital One says if you’re not satisfied with a dispute outcome, the message you receive will explain how to appeal. Read it carefully. The appeal window can be short.

Not sure if that text or call was actually from the bank? Take 60 seconds to scan the message details with the Unscammed Scam Verification Tool to confirm if you are dealing with a fraudster before you reply.

Evidence Capital One May Need to Investigate Scam Disputes

A strong case is built on documentation. The more concrete detail you can show, the faster an investigator can connect the dots.

Evidence

Why it helps

Transaction screenshot

Shows amount, merchant, date, and account

Statement line item

Confirms the posted charge

Card or account details affected

Helps identify the product involved

Merchant communications

Supports dispute attempts

Receipts or invoices

Shows what was purchased or promised

Photos of product or service issues

Helps with goods-or-services disputes

Scam texts or emails

Shows phishing, impersonation, or pressure tactics

Website URLs

Helps document fake merchant or fake bank pages

Call logs and phone numbers

Helps show impersonation attempts

Timeline of events

Makes the case easier to review

FTC, IC3, or police report numbers

Adds external documentation

Proof of account lockdown steps

Shows timely mitigation

One detail people consistently miss is that if the scammer sent you a one-time passcode by text to confirm the removal of a fraudulent charge, you must save that text message. It is much more than just embarrassing context. That message is direct evidence of how the scam worked, showing the exact timeline and tactics used to bypass security. Bank investigators see these digital patterns repeatedly, and having the precise text can help them track the source and strengthen your case.

How Long Does Capital One Take to Refund Scam Transactions?

The exact timeline for a Capital One scam refund depends entirely on your account type and whether you are filing a fraud claim or a transaction dispute. While the bank often issues a temporary credit within 10 business days, a final, permanent determination takes much longer.

Credit Card Fraud Claims (Up to 90 Days): If someone used your credit card without your permission, Capital One takes up to 90 days to investigate the unauthorized charges.

Credit Card Disputes (Up to 90 Days): If you authorized the transaction but were scammed by the merchant, Capital One concludes its investigation within 90 days. Temporary credits issued during this window are conditional and can be reversed if the bank finds the charge valid.

Debit Card Disputes (90 to 120 Days): If a scammer drains money from your checking account via your debit card, the resolution process stretches between 90 and 120 days. Capital One notes that resolving a debit issue through them can take up to four months, which is why working directly with the merchant is often the fastest route if the money is already gone.

Capital One Zero Liability Policy for Scam Victims Explained

Capital One states that credit card customers are not held responsible for unauthorized charges under its zero liability protection policy. While that sounds absolute, the practical application requires a clear understanding of specific banking terms.

Zero liability protection relies strictly on the word unauthorized. If someone steals your card details and runs up charges without your consent, you are looking at a textbook fraud case. However, if you handed over information or approved a transaction yourself, even because a scammer completely misled you, the bank’s analysis gets far more complicated. Claims are always reviewed on a case-by-case basis, and the outcome depends entirely on what the investigator finds.

For debit cards, Capital One’s banking fraud protection policy states that customers are not responsible for unauthorized charges if they report the incident in a timely manner, noting that all claims are subject to verification. The phrase timely manner carries immense legal weight here, making immediate reporting vital.

Several practical realities affect how these claims play out during an investigation:

Approving a transaction to cancel it still registers as an official approval. The common scam where a caller walks you through accepting a large charge framed as a fraud removal step lands squarely in this gray zone. You must be completely transparent with the investigator that you were deceived into taking the action, rather than stating you authorized the payment knowingly.

Sharing one-time passcodes by phone significantly weakens your claim. If you typed a code from a Capital One text alert into a third-party website or read it aloud to a caller, the bank’s system logs it as a verified action performed by the account holder. While recovery is not impossible, the burden of proof shifts heavily to you.

Debit fraud is handled differently than credit card fraud. Federal consumer protections for debit accounts are fundamentally weaker, and the stolen money is already missing from your checking account while the bank reviews the case.

A temporary credit is not a final refund. Capital One often issues a provisional credit during the active investigation but will reverse it immediately if the case is decided against you. You should avoid spending those funds until the bank officially closes the file.

Authorized users complicate the recovery process. A charge made by someone you willingly added to the account, even if they violated your trust or used the card in a way they were not supposed to, is generally treated by the bank as an authorized transaction.

Capital One Fraud Alert vs. Credit Freeze: Which Is Better After a Scam?

Option

What it does

Best for

Fraud alert

Tells lenders to take extra steps to verify your identity before opening credit

Suspected identity theft or temporary concern

Credit freeze

Blocks new credit accounts from being opened until you lift it

Stronger protection after exposed SSN or confirmed identity theft

Both

Freeze blocks access; alert adds verification language

Higher-risk identity theft cases

Understanding Fraud Alerts

A fraud alert acts as a warning flag on your credit file. It allows lenders to see your credit report but legally obliges them to take reasonable steps to verify your identity, usually by calling you directly at a number you provide, before approving any new loans or credit cards.

The Activation Rule: You only need to contact one of the three major credit bureaus (Equifax, Experian, or TransUnion) to activate a fraud alert. Federal law requires the bureau you contact to automatically notify the other two.

Duration: A standard initial fraud alert stays active for one year and can be renewed annually. If you have an official police report or an FTC identity theft report, you can secure an extended fraud alert that lasts for seven years.

Best For: Consumers who plan to apply for legitimate financing, such as a car loan, a mortgage, or a new phone plan, in the near future and want protection without completely blocking the application process.

Understanding Credit Freezes

A credit freeze, also known as a security freeze, completely seals your credit file. If a lender attempts to pull your credit history to process a new application, the bureau blocks the request entirely. Because lenders will not approve credit without reviewing your file, this step stops identity thieves completely.

The Activation Rule: You must contact all three major credit bureaus independently to place or lift a credit freeze. Freezing your report at Equifax does not automatically lock your files at Experian or TransUnion.

Duration: A credit freeze remains in place indefinitely until you actively log in or call to temporarily lift or permanently remove it.

Best For: Absolute protection. If you have confirmed that your Social Security number was compromised or you have no immediate plans to open new lines of credit, a freeze provides the highest level of security.

Comparison Grid

Feature

Fraud Alert

Credit Freeze

Primary Action

Flags your file; lenders must verify your identity.

Seals your file; blocks lenders from viewing it entirely.

Bureau Setup

Contact one bureau; they notify the other two.

You must contact all three bureaus individually.

Standard Lifespan

Expires after 1 year unless renewed manually.

Permanent until you actively choose to lift it.

Lending Impact

Does not stop applications; may add a brief verification delay.

Completely blocks new approvals until you unfreeze your file.

Overall Cost

100% Free.

100% Free.

Neither option harms your credit score, and neither tool stops a thief from making fraudulent charges on an existing Capital One credit or debit account. You must still monitor your active credit card statements independently while these broader identity protections are in place.

How to Escalate a Denied Capital One Fraud Claim

Receiving a claim denial from Capital One can be frustrating, but it does not have to be the final word. The secret to a successful escalation is recognizing that the initial customer service line rarely has the authority to overturn a decision. To reverse a denial, you must systematically elevate your case through the proper channels using a clear, evidence-based approach.

Follow this step-by-step framework to appeal a denied Capital One fraud claim or transaction dispute:

Analyze the exact denial reason: Review the decision letter or online message carefully. The specific reasoning dictates your next move, and the stated appeal window is the firm deadline you must meet.

Verify the case classification: Check whether Capital One categorized your claim as fraud, a transaction dispute, or something else. Misclassification is a primary reason claims fail. For instance, a scam payment filed as fraud might be rejected because you technically authorized the charge, whereas filing the exact same facts as a billing dispute might succeed.

Compile new documentation: Gather any evidence you missed during the initial submission. This includes screenshots of messages, receipts, or emails that support your case.

Build a chronological timeline: Investigators rely heavily on easy-to-follow facts. Create a clear, ordered timeline detailing exactly when the scam occurred, when you noticed the charge, and when you contacted the bank.

Submit an official appeal: Use the specific instructions provided in your Capital One decision notice. Do not open a brand-new claim, as doing so can reset your investigation timeline and weaken your existing case file.

Demand a senior specialist escalation: Call the number on the back of your card and explicitly ask to speak with a supervisor or a senior fraud specialist. Frontline agents typically run your file back through the same automated system that triggered the initial rejection. Do not accept a generic resubmission from a tier-one representative as a true human review.

Update federal law enforcement reports: If your case involves an online scam or identity theft, file or update your reports with the FTC (IdentityTheft.gov) and the FBI IC3 portal (ic3.gov). Include your Capital One case number directly in these filings to link the official records.

File a CFPB complaint: If Capital One refuses to cooperate despite clear evidence, submit a formal complaint through the Consumer Financial Protection Bureau portal. The CFPB process legally requires financial institutions to respond within 15 days and provide a final resolution within 60 days.

Contact the OCC for banking policy violations: For deep structural issues or unfair account freezes, you can lodge a complaint with the Office of the Comptroller of the Currency, which serves as Capital One’s primary federal regulator.

Maintain a rigorous paper trail: Document every single case number, call date, and written response. Whenever you speak to a representative, log the exact time of the call, the agent’s name, and their employee ID number. If an agent makes a verbal promise that contradicts your written denial, ask for that statement in writing immediately.

How to File a Parallel FBI IC3 Report After a Capital One Scam

The FBI’s Internet Crime Complaint Center, located at ic3.gov, is the primary federal channel for reporting cyber-enabled financial fraud. Filing an IC3 report is critical if your Capital One scam involved any of the following digital tactics:

Online phishing schemes or fake Capital One websites and apps

Account takeovers or business email compromise

Tech support scams or fraudulent bank representatives calling from spoofed numbers

Investment and romance scams

Unauthorized payment scams that routed money through wire transfers, Zelle, or Cash App

Capital One’s official security education guidelines explicitly recommend reporting cyber scams to both the FTC and the FBI to assist law enforcement in tracking down digital criminal networks.

Two Critical Realities of the IC3 Filing Process

Before submitting your complaint, you must understand how the FBI processes these reports:

The IC3 is an aggregation database, not a direct recovery service. The IC3 does not personally investigate individual claims or manually return your stolen funds. Instead, it serves as a central intake hub. Intelligence analysts look for data patterns across thousands of complaints. While a single isolated report might not trigger an immediate response, linking your report with hundreds of others naming the exact same phone numbers, fake employee names, or digital wallet addresses is how federal agencies build major criminal cases.

The Recovery Asset Team (RAT) operates on a strict timeline. The IC3 features a specialized division called the Recovery Asset Team that coordinates directly with financial institutions to freeze and claw back fraudulent domestic wire transfers. However, this team primarily intercepts large-scale wire fraud, typically over $50,000, and their success rate drops precipitously after 72 hours. If a scammer tricked you into wiring a large sum from your Capital One account, you must file an IC3 report within hours to give the RAT a viable window to act. For instant-settlement networks like Zelle or Cash App, these clawback options are practically nonexistent.

Essential Evidence to Include in Your FBI Report

To help investigators connect your case to broader active fraud rings, your submission should be as granular as possible. Gather and include the following details:

Transaction specifics: Exact dollar amounts lost, Capital One transaction IDs, and precise dates and times adjusted to your local time zone.

Scammer contact details: Inbound phone numbers, fake employee names, spoofed email addresses, and the complete destination URLs of any lookalike bank portals.

Financial routing endpoints: Destination bank routing numbers, recipient account numbers, or cryptocurrency wallet addresses provided by the scammer.

Cross-reference numbers: Your active Capital One fraud case number and your FTC reference number if you have already filed one.

Practical IC3 Filing Notes Most People Miss

No account registration is required: Anyone can submit a public complaint directly at ic3.gov. However, creating a voluntary portal account allows you to save active drafts and append new details to your file later.

Never file duplicate reports for the same incident: The FBI explicitly requests that victims do not submit multiple entries for a single scam event, as duplicates clog the automated pattern-matching system. If you uncover new evidence after submitting, log back into your file to update the existing record.

Secure your official IC3 complaint number: You will receive a unique tracking number immediately upon submission. Keep this code safe, as Capital One fraud investigators often request it to validate your claims, and the FTC system can use it to link parallel identity theft profiles.

International jurisdiction limitations are expected: The IC3 is designed for U.S. residents or crimes targeting U.S. financial interests. If an international scammer targeted you while you were on U.S. soil, the IC3 is your best recourse, as local police departments lack the jurisdiction to investigate overseas digital fraud.

Expect total radio silence from investigators: The FBI rarely contacts individual filers unless an agent specifically requires your documentation for an active prosecution. A lack of personal follow-up is standard operational procedure and does not mean your file has been dismissed.

If your Capital One incident involved full identity theft, such as a criminal using your Social Security number to open entirely new lines of credit, you must also file a parallel report at IdentityTheft.gov. That system generates a formal FTC Identity Theft Report, which Capital One requires to legally clear fraudulent debts from your name.

A Note on the Cash App and Zelle Pattern

This is one of the most damaging Capital One scam variants in circulation, and it almost never ends in a refund.

The pattern is that someone calls or texts pretending to be Capital One’s fraud department. They convince you a charge needs to be reversed. They tell you to move money from your Capital One account into Cash App, Zelle, or a wire transfer, claiming they’re “creating a new account for you to deposit into.”

That new account belongs to them, at a completely different bank. Victims report losing thousands this way in a single afternoon. The scammer kept him on the line through the entire transfer, calmly walking him through the steps.

A few specifics worth knowing:

Zelle transfers settle instantly and are usually irreversible. Banks often deny these claims because you initiated the transfer yourself, making it “authorized” in their eyes. While regulatory pressure has pushed some banks to reimburse specific impersonation scams, coverage is inconsistent, so you must report the transfer the same day for any chance of a recall.

Cash App offers virtually no consumer protection. Peer-to-peer transfers are not covered by standard banking regulations, and completed payments cannot be canceled. Your only option is asking the scammer for a refund, which they will not grant.

Wire transfers require immediate action to recall. The FBI IC3 Recovery Asset Team can only attempt to freeze and claw back domestic wires if you file a report within a strict 72-hour window.

Destination accounts are closed within hours. Scammers quickly route stolen funds through multiple mule accounts before converting the cash to cryptocurrency or withdrawing it, meaning the money is usually gone before an investigation even begins.

If anyone who is claiming to be your bank asks you to move money to “protect” it, hang up. Banks don’t do that. Capital One doesn’t do that. It’s always a scam.

How Recovery Services Can Help With Capital One Fraud Claims

No legitimate service can guarantee a Capital One scam refund or offer a secret back-channel into the bank’s internal departments. If you need help organizing your case, a legitimate support tool or legal professional should only be used to:

Identify if your situation requires a Capital One fraud claim or a standard billing dispute.

Organize your screenshots, bank statements, and communication timestamps into a clear chronology.

Route your documentation to official federal channels, such as a report Capital One scam to IC3 submission.

Help you avoid unverified support phone numbers and suspicious follow-up messages.

For massive financial losses exceeding $50,000, real asset recovery is handled exclusively by the FBI’s Recovery Asset Team through the official ic3.gov portal, never by private third-party agents. Never share your online banking password, PIN, or one-time codes with anyone claiming they can recover your money.

How Recovery Scammers Target Capital One Customers

The Spoofed Callback: They instruct you to call a number that plays a fake, institutional greeting mimicking the Capital One fraud reporting line.

Fake Government Affiliation: Fraudsters pretend to represent federal agencies like the FTC, FBI, or CFPB. Legitimate government entities never contact scam victims out of the blue to recover money, nor do they charge fees.

The “Release Fee” Trap: They falsely claim they have already located your funds but require an upfront tax, verification deposit, or administrative fee to release them.

Exploiting One-Time Codes: They will ask you to read back a verification text code to “confirm your identity,” using the exact same tactic that compromised your account in the first place.

Untraceable Payment Demands: They demand payment via cryptocurrency, gift cards, or overseas wire transfers.

Artificial Urgency: They pressure you with short deadlines, claiming they can only hold your recovered funds for a few hours.

If someone claims they can recover your Capital One funds, check the message with Unscammed before you reply, pay, or share any personal information.

Capital One Fraud Reporting Checklist

Immediate Action (First 30 Minutes)

Cut contact: Cease all communication with the scammer immediately.

Secure credentials: Do not click links or share one-time passcodes, even if they are framed as a security fix.

Freeze the account: Lock the compromised card instantly inside the Capital One mobile app.

Preserve evidence: Screenshot the transaction, caller ID, messages, and any lookalike bank web pages.

Timestamp the event: Record the exact time you discovered the fraud.

Same-Day Response (Next Few Hours)

Audit the charge: Verify if the transaction is pending or posted, and rule out authorized users or forgotten subscriptions.

Initiate the claim: File credit card fraud via the Report a problem button in the app. For debit or scam concerns, call the Capital One fraud department phone number at 1-888-464-0727 or 1-800-227-4825.

Flag money transfers: Report Zelle, Cash App, or wire transfers immediately. Domestic wire recall windows can close within 72 hours.

Update passwords: Change your Capital One banking password and your primary email password.

Short-Term Protection (First Week)

Alert federal agencies: File a report at reportfraud.ftc.gov, and submit a cyber fraud report to the FBI at ic3.gov.

Protect your identity: If personal data was leaked, file a report at IdentityTheft.gov and monitor your credit files.

Secure your credit: Place a free Capital One credit freeze or fraud alert with Equifax, Experian, and TransUnion.

Ongoing Monitoring (Next Several Weeks)

Maintain a paper trail: Log all bank case numbers, denial letters, and representative employee IDs.

Review statements daily: Track your account closely for any recurring Capital One unauthorized charge.

Block recovery scammers: Ignore third-party solicitations promising a Capital One scam refund for an upfront fee.

Manage denials: If your Capital One dispute is denied, gather your timeline and submit a formal appeal before the window closes.

FAQs

How do I report fraud to Capital One?

For credit card fraud, log into the Capital One mobile app or website, select the specific transaction, click Report a problem, and complete the guided questionnaire. For debit card fraud or account compromise, call Capital One customer service immediately at 1-888-464-0727 or 1-800-227-4825.

What is the Capital One fraud department phone number?

Capital One routes fraud claims based on the account type. Call 1-888-464-0727 to report debit card fraud, and call 1-800-227-4825 to report active scams or full account compromise. Credit card holders can also call the dedicated support line printed directly on the back of their physical card. Never dial phone numbers found in unexpected text alerts, search engine advertisements, or unsolicited cold calls.

How long does Capital One take to investigate fraud?

Capital One credit card fraud claims and billing disputes are typically resolved within 90 days. For debit card disputes involving a merchant transaction, the bank’s internal resolution process can take up to four months to fully finalize.

Does Capital One have zero liability for scam victims?

Capital One provides complete zero liability protection for credit card customers, meaning you are not held responsible for unauthorized charges. However, this policy does not guarantee an automatic refund if a scammer successfully tricks you into authorizing or sending a payment yourself. The bank evaluates the specific facts of each claim during the investigation.

Should I file a fraud claim or a dispute with Capital One?

File a fraud claim if a transaction occurred entirely without your permission or knowledge. File a merchant dispute if you willingly authorized the payment but experienced a transaction problem, such as a missing shipment, a duplicate billing error, or a service that failed to match what was promised.

Is a fraud alert or credit freeze better after a Capital One scam?

A fraud alert requires lenders to verify your identity before granting new credit, making it ideal if you plan to borrow money soon. A credit freeze offers stronger protection by completely locking your files against new applications. The FTC provides both security tools for free, and identity theft victims frequently combine them for maximum protection.

How do I escalate a denied Capital One fraud claim?

Review your formal denial letter to check the deadline, fix any gaps in your evidence, and follow the exact appeal directions provided in the notice. Call the number on your card to request a formal escalation to a senior fraud specialist. If cyber fraud occurred, file updated reports through the FTC and IC3 portals, and submit a complaint to the CFPB if the issue remains deadlocked.

Should I file an IC3 report after a Capital One scam?

Yes. You should file an official report at ic3.gov if the incident involved digital phishing, account takeovers, fake banking portals, impersonation, or any internet-enabled crime. Ensure your submission includes precise transaction logs, screenshots of conversations, scammer contact details, and your active Capital One case number.

A Final Word

Successfully navigating Capital One report fraud protocols comes down to three decisive actions: move fast, choose the correct reporting path, and document every detail.

True unauthorized charges, merchant billing disputes, peer-to-peer scam payments, and total identity theft are fundamentally different issues. Confusing them on the phone is the number one reason claims get rejected. When fraud strikes, execute your defense in this exact order:

Lock the account instantly to stop the bleeding.

Preserve every piece of digital evidence, including text messages and screenshots.

Report through official Capital One channels, matching your story perfectly to the correct claim type.

File external law enforcement reports with the FTC and IC3 the moment a scam spills past a single transaction.

Hang up on recovery agents. Anyone guaranteeing they can bypass bank security to win your money back for a fee is just running the next scam.

Falling victim to these crimes is not a reflection of your intelligence. These syndicates deploy highly sophisticated psychological scripts explicitly engineered to trap smart, careful people. The fact that you are actively arming yourself with this strategy means you are already breaking their script, taking control, and outsmarting the scammer.

Being scammed is disorienting, and it can happen to anyone, including careful, smart people who do everything right most of the time. If your stomach just dropped, take that as your cue to act, not to freeze.

Family identity theft is not just one person's credit card being stolen. In a single household you might have children with unused Social Security numbers, elderly parents targeted by phone scams, adults exposed in data breaches, and shared devices or accounts that create extra risk. Each person faces a different threat, and protecting the family means covering all of them.

Share:

Share: