What To Do if You Get Scammed: A Step-by-Step Guide:

Being scammed is disorienting, and it can happen to anyone, including careful, smart people who do everything right most of the time. If your stomach just dropped, take that as your cue to act, not to freeze.

Share:

This is a clear, in-order checklist of what to do if you get scammed, starting with the moves that matter most in the first hours. Work through it from the top. The earlier steps are the time-sensitive ones.

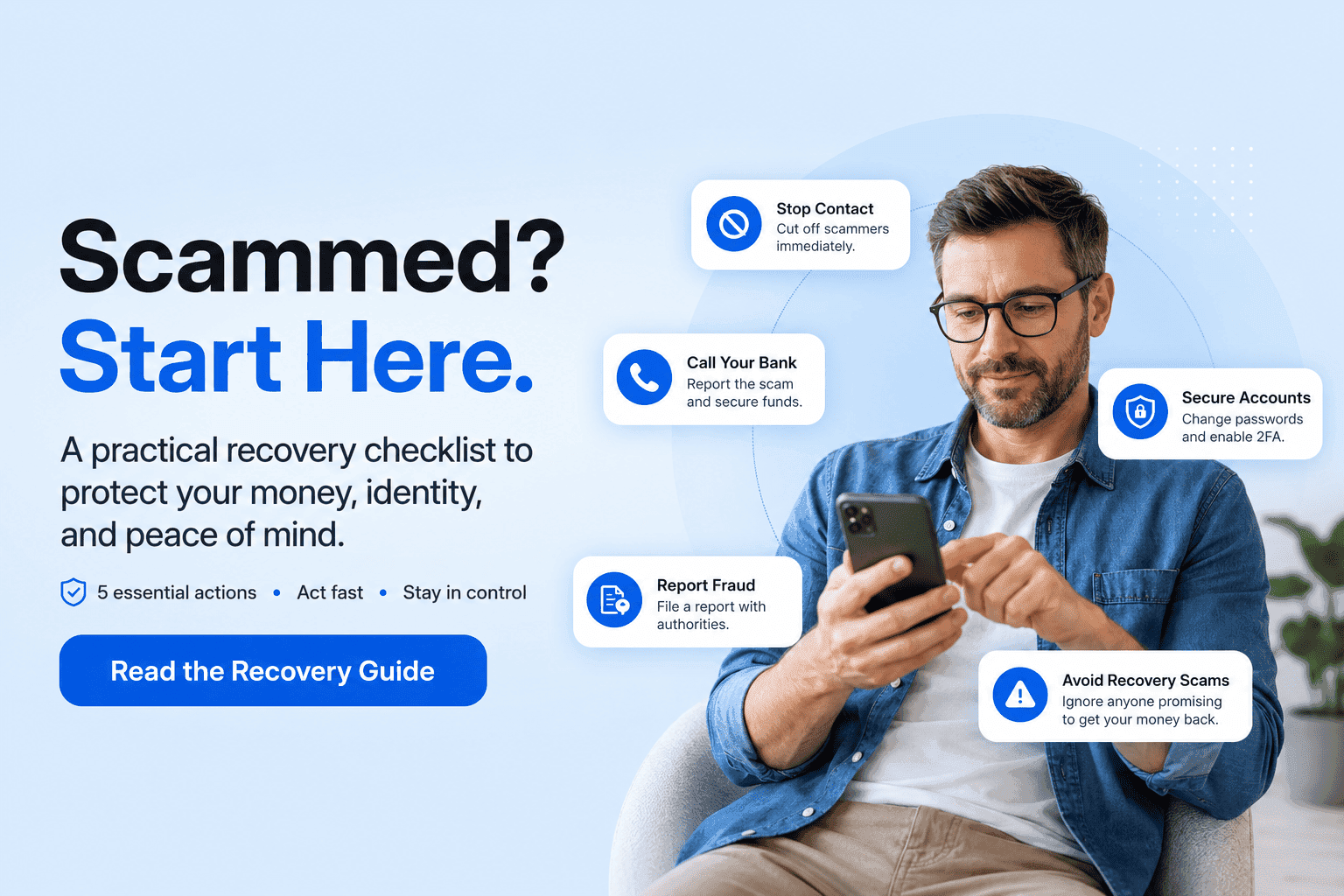

If you only do one thing right now, do these five:

Stop all contact with the scammer and cut off any access they have.

Contact your bank or payment provider and ask them to reverse or refund the payment.

Change your passwords, starting with email and banking, and turn on two-factor authentication.

Watch for follow-up “recovery” scams. Anyone promising to get your money back for an upfront fee is the second scam.

First, take a breath, then move fast

Two things are true at once. You need to move quickly, and you should not spiral. Speed and calm are not opposites here, and knowing what to do if you get scammed in advance is half the battle won.

Why the rush? Because the sooner you act, the better your chances of stopping a payment, reversing a transaction, or limiting the damage. Some money may already be gone, but it is always worth asking the company you paid whether there is a way to get it back. That single question, asked fast, is sometimes the difference.

Now the part nobody says out loud enough: this is not your fault, and you are not stupid. Scammers run these schemes thousands of times until the script is airtight. Telling someone, your bank, a family member, the authorities, is a sign of strength, not embarrassment. Silence is what scammers count on. So is shame. Don’t give them either.

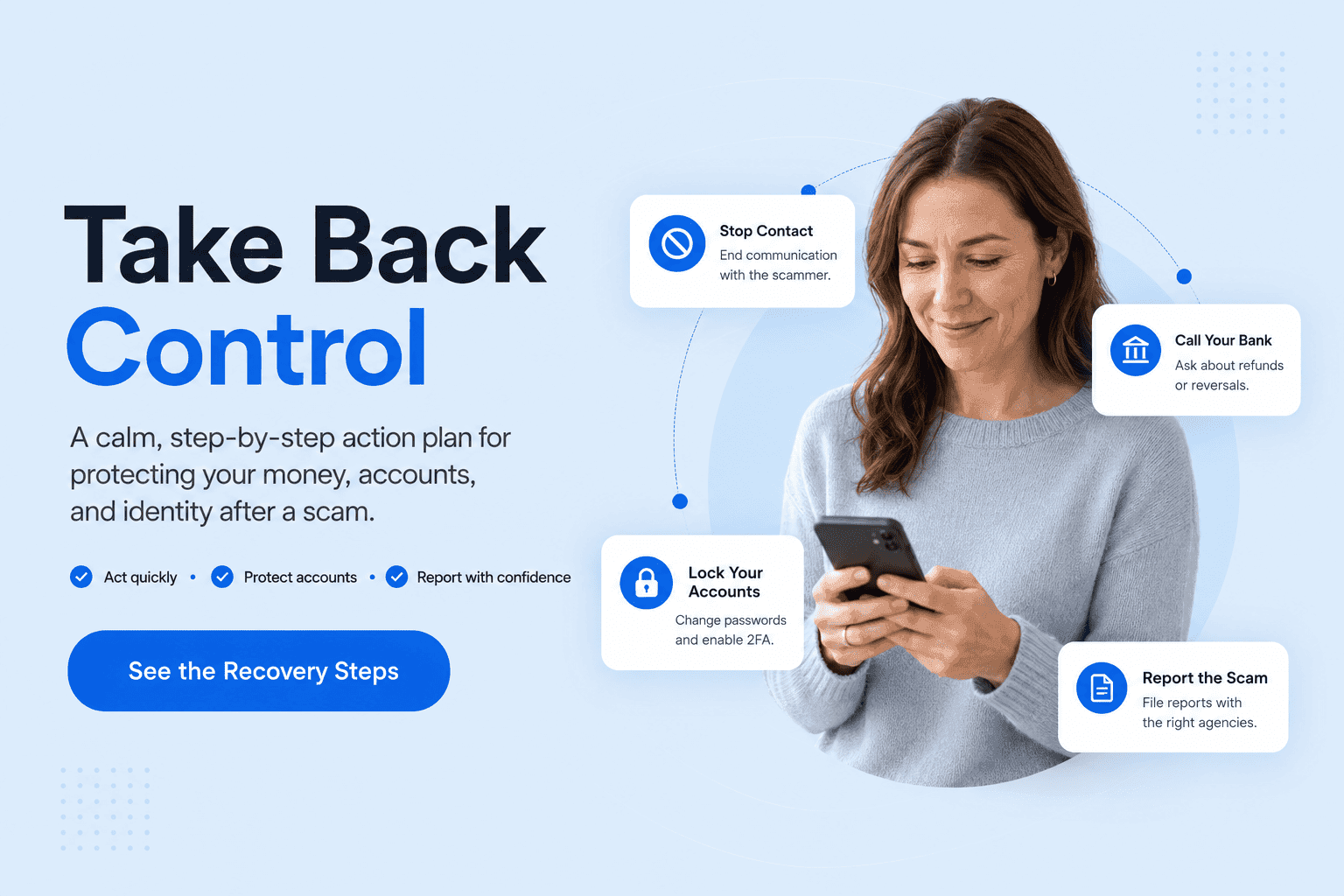

Step 1: Cut off the scammer’s access

Before you try to recover anything, close the door. This is the very first thing on the list of what to do if you get scammed, because every minute the scammer keeps access is a minute they can do more damage.

Stop all contact and don’t send another cent. No more payments. No “unlock” fee, no “verification” charge, no “tax” to release your funds. Scammers escalate the moment they sense a live, paying target, so every reply keeps the hook in. Stop responding entirely.

If they got into your device, treat it as compromised. Disconnect it from the internet. Uninstall any remote-access app they had you install, the kind with names like AnyDesk or TeamViewer. Run a security scan, and change your passwords from a different, clean device so you are not typing new credentials into a machine they may still be watching.

Change your passwords and turn on two-factor authentication. Start with email and banking, since those are the keys to everything else. Use a unique password for each account. If you reused a password that may have been exposed, change it everywhere it was used. Turning on two-factor authentication adds a second lock even if a password leaks. For more on protecting your information before it gets shared, how to avoid sharing personal information is worth a look.

Step 2: Try to get your money back

This depends mostly on how you paid. The universal rule comes first: contact the company you used to send the money as fast as you can, and ask them to reverse or refund it. The FTC’s guidance on what to do if you were scammed breaks this down by method, and so does the table below.

How you paid

First move

Reversal odds

Credit card

Call issuer, report fraud, dispute the charge

Good if reported fast

Debit card

Call your bank immediately, dispute the charge

Good, but act faster (money already left your account)

Wire transfer

Contact the wire company and your bank to recall it

Time-critical

Gift card

Call the card brand, report the scam, ask for a refund

Low, but worth trying

Payment app

Report the fraud in-app and to your linked bank

Low, app-to-app is hard to reverse

Cryptocurrency

Report to the exchange, FTC, and IC3

Very low, rarely reversible

Mailed cash / money order

Contact USPS or the money-order issuer to stop it

Low, only if caught early

If you paid by credit or debit card, call your bank or card issuer, report the fraud, and dispute the charge. This is a chargeback, and it is one of your stronger tools. Debit pulls money straight out of your account, so move even faster than you would with a credit card.

If you used a wire transfer through Western Union, MoneyGram, or a bank wire, contact the wire company and your bank right away and ask them to reverse the transfer and flag it as fraudulent. Wires are fast and hard to undo, so minutes matter.

If you bought gift cards, contact the company that issued the card, the brand printed on the front, tell them it was used in a scam, and ask for a refund. Keep the card and the receipt, because they will need the numbers. The FTC’s gift card scam guidance lists the contact lines for the major brands.

If you used a payment app like Zelle, Venmo, Cash App, or PayPal, report the fraudulent transaction inside the app and to the bank linked to it, and ask whether it can be reversed. Be realistic: app-to-app transfers are hard to claw back once sent, which is exactly why reporting fast matters. If Zelle was involved, our step-by-step on how to report a Zelle scam covers the bank timelines and when to escalate. For purchases on a marketplace, what to do if you get scammed online shopping walks through disputes and refunds.

If you sent cryptocurrency, report it to the exchange or wallet provider and to the FTC and FBI’s IC3 cryptocurrency unit. Be honest with yourself here: crypto is rarely reversible, as the FTC’s cryptocurrency scam guidance explains, but reporting can aid tracing and warn others. If you are choosing where to file, our comparison of crypto scam reporting tools helps.

If you mailed cash or a money order, contact the carrier, USPS or the money-order issuer, to try to stop delivery or cancel it before it is collected.

Step 3: Lock down your identity

Did you share personal information, a Social Security number, bank or account numbers, a login, or your date of birth? If so, treat this as potential identity theft and act on it now.

Go to IdentityTheft.gov and follow the recovery plan. This is the federal government’s one-stop resource for identity theft victims. It builds a personalized recovery plan and even provides sample letters and checklists. It is the single best starting point when personal information has been exposed.

Freeze your credit and add a fraud alert. These are two different tools. Place a credit freeze with all three bureaus, Equifax, Experian, and TransUnion, since a freeze must be set at each one separately. For a fraud alert, you only need to contact one bureau, which must then notify the other two. The FTC’s guide to credit freezes and fraud alerts explains both, and our breakdown of identity fraud vs identity theft covers which protection fits your situation.

Secure the accounts that were exposed. Call your bank to flag or lock affected accounts, reissue cards, and change your online-banking credentials. If your identity was used to open accounts or you need an official record, filing an identity theft police report creates a paper trail that helps with disputes later.

Step 4: Report the scam (it matters more than you think)

Reporting can feel like pointless paperwork when your money is already gone. It is not. Reporting may not get your money back directly, but it creates an official record, helps law enforcement identify patterns, and can support banks, investigators, and future enforcement action. Here is where to send it.

Report to the FTC at ReportFraud.ftc.gov, the central US fraud report. Your report joins a database that law enforcement across the country uses to spot trends and build cases.

Report online crime to the FBI through IC3, using the IC3 complaint form for internet-enabled scams, especially larger losses, wire fraud, and crypto cases. In some situations, fast IC3 reporting can help freeze stolen funds.

File a local police report if your bank, insurer, platform, or identity-theft recovery process asks for one, or if you have specific information about the scammer. Keep the report number. For identity theft, an FTC Identity Theft Report from IdentityTheft.gov is often enough for many recovery steps, though a local police report can still help in some cases.

Tell your state attorney general’s office. State AGs track local fraud and can advise on your rights and next steps. You can find yours through the NAAG directory.

Report to the platform or impersonated company. The marketplace, bank, or brand that was spoofed can often warn others and sometimes assist. If you are not sure where each type of fraud goes, the government’s where to report a scam hub and our roundup of top scam reporting platforms both map it out.

Reporting to several agencies at once is a lot to manage when you’re already shaken. Unscammed walks you through reporting to the right bodies and keeps your case organized in one place.

This is the step most guides skip, and it catches people at their lowest moment.

After the first scam, fraudsters buy and trade “sucker lists” of prior victims, then circle back promising to recover your lost money for an upfront fee. The pitch sounds like rescue. It is the second scam. Here is the rule that cuts through all of it: a legitimate agency will never ask you to pay to get your money back. The FTC’s guidance on refund and recovery scams lays out the pattern.

If someone contacts you out of the blue offering recovery, especially asking for a fee, a “tax,” gift cards, or crypto, walk away and report them. We cover the full playbook in how to avoid fake scam recovery services.

How to recover, emotionally and financially

The aftermath is its own thing. Anger, embarrassment, anxiety, replaying the moment you clicked or paid: all of it is normal, and none of it means you failed. Tell a trusted person. Isolation is the scammer’s ally, and saying it out loud takes away its power.

On the practical side, a short routine helps you feel in control again. Monitor your bank and credit card statements closely for a few months. Keep everything about the scam in one folder, screenshots, emails, receipts, report numbers. Set up account alerts so you hear about any new activity fast. Small, steady steps rebuild the ground under your feet.

How to protect yourself going forward

You already learned the hardest lesson. A few habits keep it from happening twice.

Verify before you pay, using a number or address you looked up yourself, not one they gave you. Never move money to “protect” it, because real institutions never ask for that. Slow down whenever something feels urgent, since urgency is the scammer’s favorite lever. Use unique passwords with two-factor authentication. And if you are job hunting, where scams are common, how to know if a job is a scam is a useful starting point.

Frequently asked questions

What to do if you get scammed and you already paid?

Stop all contact with the scammer and don’t send any more money. Then contact the bank or service you paid through and ask them to reverse or refund it, change your important passwords, and report the scam to the FTC at ReportFraud.ftc.gov. Acting within the first hours gives you the best chance.

Can I get my money back after being scammed?

Sometimes, and it depends mostly on how you paid. Credit and debit cards and wire transfers have the best reversal odds if you report fast, while gift cards, payment apps, and crypto are harder but still worth reporting right away. Always ask the company you used to send the money to reverse it.

Who do I report a scam to in the United States?

Report to the FTC at ReportFraud.ftc.gov, and for internet-based scams also file with the FBI’s IC3 at ic3.gov. Consider a local police report, since some banks require one, and notify your state attorney general’s office.

I gave a scammer my Social Security number, now what?

Treat it as identity theft. Go to IdentityTheft.gov for a step-by-step recovery plan, place a credit freeze with all three bureaus or a fraud alert with one, and monitor your accounts and credit closely.

What should I do if I paid with a gift card?

Contact the company that issued the gift card right away, tell them it was used in a scam, and ask for a refund. Keep the card itself and your purchase receipt, since you will need the numbers.

A scammer has remote access to my computer, how do I lock it down?

Disconnect the device from the internet, uninstall any remote-access app they had you install, run a security scan, and change your passwords starting with email and banking from a different, clean device.

How do I avoid being scammed a second time?

Be very wary of anyone who contacts you promising to recover your lost money for an upfront fee, because that is a common follow-up scam. A legitimate agency will never ask you to pay to get your money back.

How long do I have to act after being scammed?

As soon as possible, ideally within hours. Payment reversals, card disputes, and wire recalls become much harder as time passes, so contact your bank and the authorities right away.

You’re not on your own from here

Knowing what to do after being scammed is the part that turns panic into a plan. You cannot undo the moment it happened, but you can control the next few hours, and those hours matter most. Cut off access, chase the money, lock down your identity, report it, and stay alert for the recovery scam that often follows.

You don’t have to handle the aftermath alone. Unscammed helps you report the scam, protect your identity, and watch for follow-up fraud.

Being scammed is disorienting, and it can happen to anyone, including careful, smart people who do everything right most of the time. If your stomach just dropped, take that as your cue to act, not to freeze.

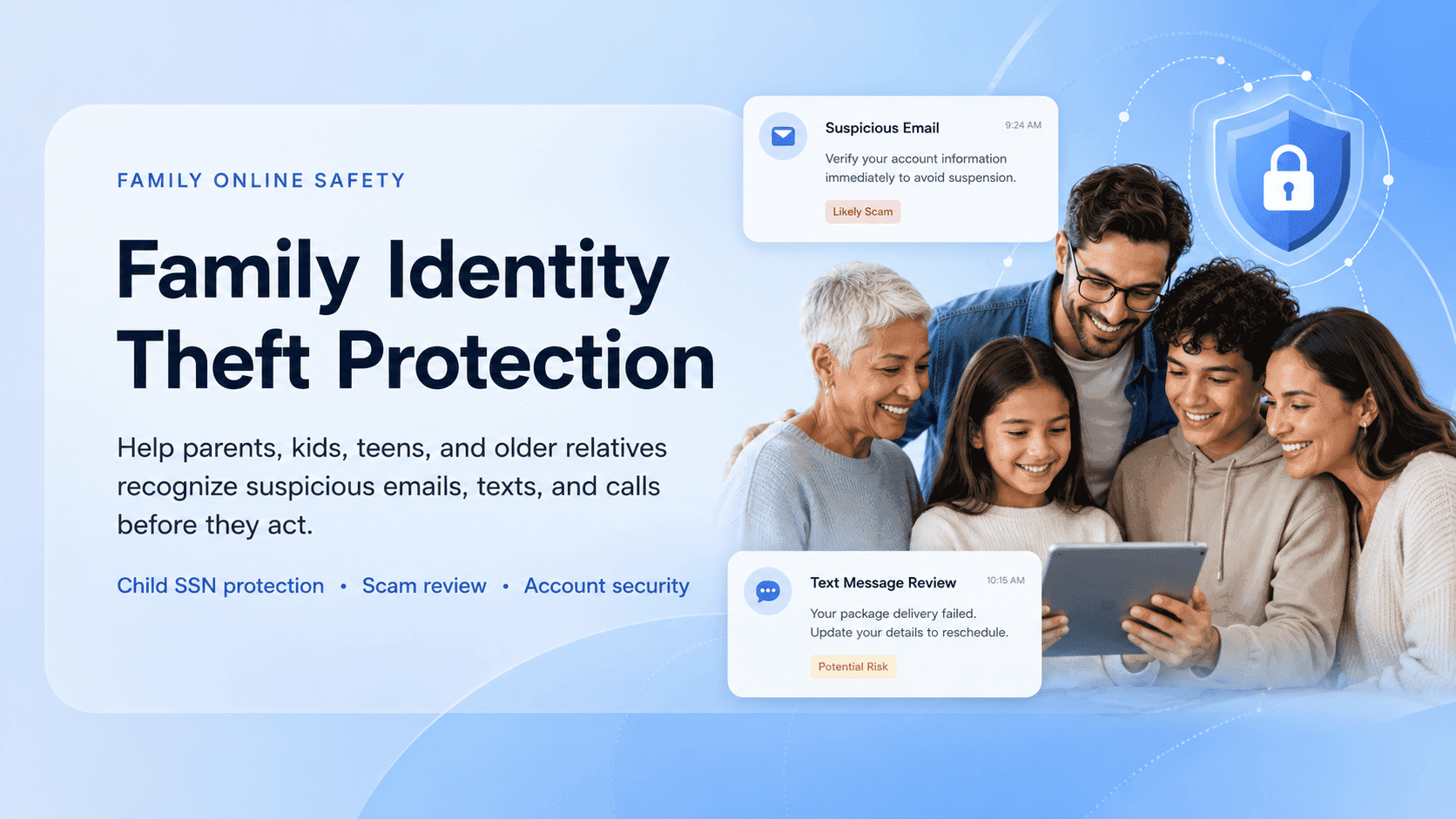

Family identity theft is not just one person's credit card being stolen. In a single household you might have children with unused Social Security numbers, elderly parents targeted by phone scams, adults exposed in data breaches, and shared devices or accounts that create extra risk. Each person faces a different threat, and protecting the family means covering all of them.

Share:

Share: