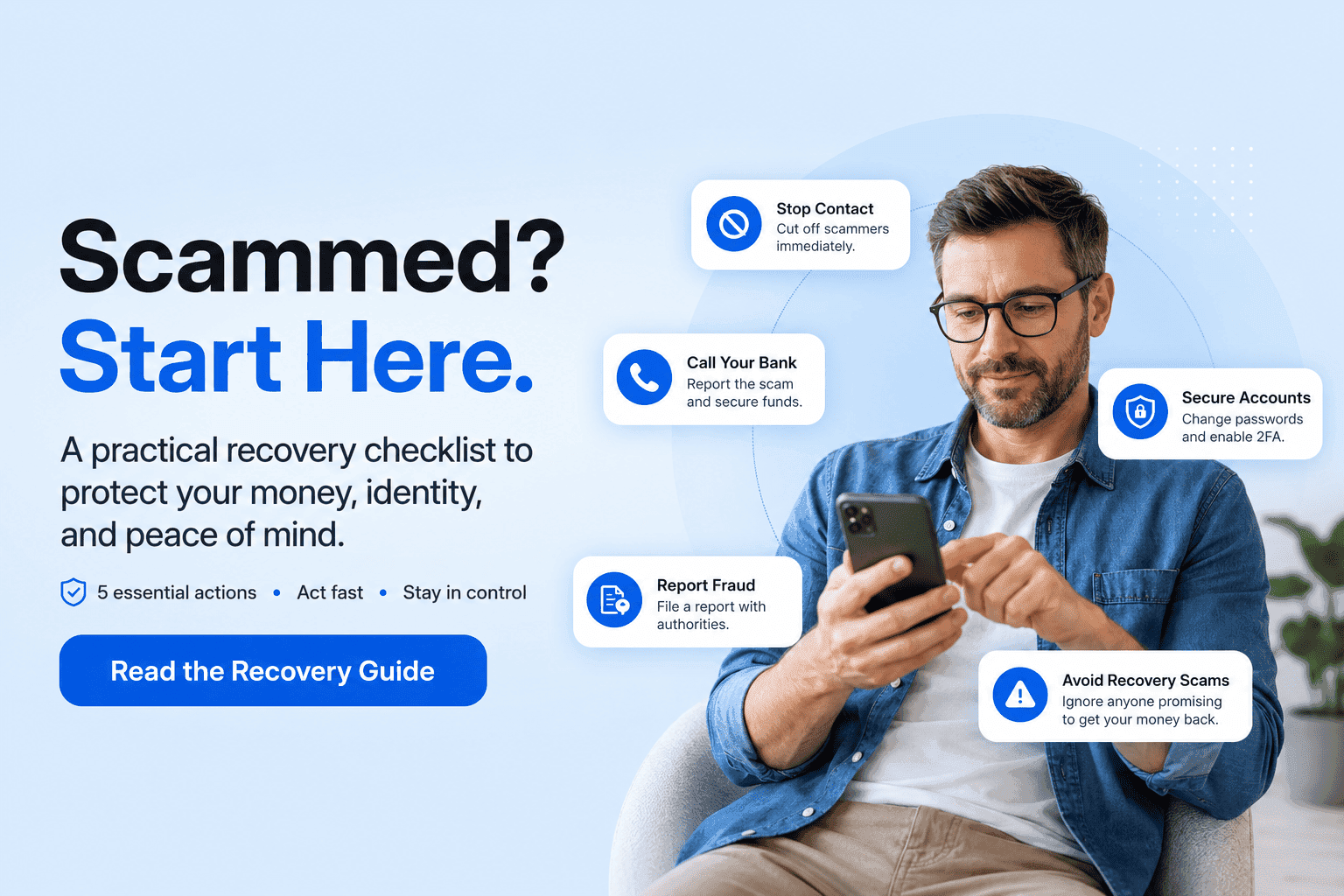

How to Report a Zelle Scam and Recover Money: Bank Steps, Timelines, and Escalation Options:

If you were scammed on Zelle, report it immediately to your bank, file a fraud dispute, document your evidence, and escalate to regulators if your claim gets denied. A scam reporting platform helps you build a stronger recovery case from the start.

You sent the payment. Then you realized something was wrong. Maybe the seller vanished. Maybe the "bank rep" who asked you to transfer funds was not from your bank at all. Maybe someone got into your account and moved money without you knowing.

Whatever happened, act now. Zelle payments move instantly and they are difficult to reverse, but that does not mean recovery is impossible. It means the next few hours matter more than you think.

This guide covers every step: how to report a Zelle scam, how to dispute the transaction, what your bank is required to investigate, and what to do if they say no. Start by documenting your evidence with Unscammed's scam reporting service before you call your bank.

Key Takeaways

1. Zelle payments are difficult but not impossible to reverse

2. Reporting quickly improves your recovery chances significantly

3. Banks require clear documentation to process fraud disputes

4. Escalation options exist if your refund is denied

5. A scam reporting tool helps you build and organize evidence fast

What to Do Immediately After a Zelle Scam

The first hour after a Zelle scam matters most. Zelle processes payments instantly between bank accounts, which means there is no holding period to catch a fraudulent transfer. But fast action on your end can still make a difference.

Step

Action

Contact your bank

Call the fraud department and report the transaction immediately

Freeze or lock your account

Prevent any further unauthorized transfers or access

Document the transaction

Screenshot the payment details, date, amount, and recipient

Report to Zelle

Submit a complaint through the Zelle app or website

File a police report

Create legal documentation to support your dispute

Do not wait to see if the money comes back on its own. It will not. And every hour you delay is an hour the scammer has to move or spend those funds.

Your bank is your first and most important contact. Zelle itself does not hold funds or manage disputes directly. The participating bank where your account is held handles the investigation and any reimbursement decision.

Step

What to Do

Call the bank fraud department

Report the scam immediately. Ask for the fraud line specifically, not general customer service

Submit a written dispute

Follow up your call with a written dispute request. Get it on record

Provide documentation

Send screenshots, chat records, emails, and a clear timeline of what happened

Request a case number

You need this to track the investigation and escalate if necessary

Follow up regularly

Check in every few days. Do not assume the case is moving without you

Where exactly do you report Zelle fraud? Call the number on the back of your debit card or log into your bank's app and navigate to the fraud or dispute section. Most major banks, including Chase, Bank of America, and Wells Fargo, have dedicated fraud lines available 24/7.

Be specific when you call. Tell them the exact date, amount, and recipient. Tell them whether you authorized the payment or whether someone accessed your account without your knowledge. That distinction matters for how your bank classifies the dispute.

Can Zelle Reverse a Scam Payment?

This is the question everyone asks first. The honest answer: sometimes, but it depends on the type of fraud.

Zelle and your bank are more likely to reverse a payment when the transaction was clearly unauthorized, meaning someone accessed your account without your knowledge. They are less likely to reverse a payment when you sent the money yourself, even if a scammer tricked you into doing it.

Scenario

Reversal Possible

Unauthorized transaction (account takeover)

Often reversed

Account hacked or compromised

Often reversed

Sent to scammer voluntarily after being deceived

Harder to recover

Impersonation scam (fake bank rep, fake seller)

Sometimes reversed

Accidental payment to wrong person

Depends on bank and recipient cooperation

Does Zelle refund scams? Not automatically. The reimbursement decision sits with your bank, not with Zelle. Under pressure from the Consumer Financial Protection Bureau and new industry guidelines introduced in 2023, many banks now reimburse customers who were deceived into sending payments through impersonation scams. But this is not guaranteed, and the outcome often depends on how well you document your case.

How to Dispute a Zelle Transaction

A dispute is a formal request to your bank to investigate and potentially reverse a transaction. Here is how to do it properly.

Contact Your Bank Immediately

Call before you do anything else. The sooner the dispute is on record, the better. Ask specifically for the fraud or disputes department, and use the word "unauthorized" if your account was accessed without your permission.

Submit a Written Dispute

Follow up every phone call with something in writing. Send an email or submit through your bank's secure message center. Written disputes create a paper trail that protects you throughout the process.

Provide Supporting Evidence

The more documentation you submit, the stronger your case. Banks need to see that something fraudulent happened, and your evidence is what makes that case.

Evidence

Purpose

Transaction screenshot

Confirms payment amount, date, and recipient

Chat or text messages

Shows how the scammer communicated with you

Email communication

Demonstrates fraud intent and deception

Phone logs

Proves contact with the scammer

FTC or police report number

Adds legal weight to your dispute

Request Escalation

If the first representative cannot help, ask for a supervisor. If the bank closes your dispute without a satisfactory explanation, request a written denial. You will need it for the next step.

How Long Does a Zelle Investigation Take?

Expect the process to take weeks, not days. Here is a realistic breakdown of the typical timeline.

Stage

Typical Timeframe

Initial report accepted

Same day

Bank review begins

5 to 10 business days

Active investigation

10 to 30 days

Final resolution

30 to 90 days

Follow up every week. Banks handle hundreds of disputes at a time. A case that sits without follow-up from the victim often moves slower than one where the customer checks in regularly. Ask for status updates, write down who you spoke with, and keep notes on every call.

If 30 days pass without resolution, that is your signal to escalate.

What to Do If Your Bank Refuses a Zelle Refund

A denial from your bank is not the end of the road. You have real escalation options, and using them has worked for other victims.

Request a Written Denial

Before you do anything else, ask for the denial in writing. This document is what you need to file complaints with regulators. Some banks will push back on this. Be firm.

Escalate to a Bank Supervisor

Ask to speak with a fraud supervisor or the bank's dispute resolution team. Explain that you are prepared to file a regulatory complaint. This sometimes prompts a second review.

File a Complaint with Regulators

This is your most powerful next move. The Consumer Financial Protection Bureau (CFPB) accepts complaints at consumerfinance.gov and requires banks to respond within 15 days. The Federal Trade Commission (FTC) also accepts fraud reports. State attorneys general offices are another option, especially if the scam crossed state lines.

Submit a Police Report

A police report adds legal weight to your case and may prompt your bank to reopen the investigation. It also creates documentation you can use if you pursue civil action later.

Contact all of them. Each report adds a layer of documentation. The CFPB complaint in particular puts direct pressure on your bank because they are required to respond formally.

Can Police Help with a Zelle Scam?

Yes, in a specific and important way. Police cannot force Zelle or your bank to reverse a payment. But a police report does several things that matter.

It creates an official record of the fraud. It gives your bank a case number to attach to your dispute. It adds credibility to your claim that the transaction was not legitimate. And if your case ever moves toward civil or criminal action, it is essential documentation.

Police Report Benefit

Why It Matters

Official fraud documentation

Strengthens your bank dispute

Case number

Required by some banks for dispute processing

Investigation record

Tracks the incident formally with law enforcement

Escalation support

Needed for regulatory complaints and appeals

Some banks explicitly ask for a police report number before they will process certain types of fraud disputes. File it early so you have it ready.

You can use Unscammed's scam reporting platform to organize your evidence into a clear, structured report before you go to the police or your bank.

Zelle Scam Recovery Options

There is no single path to recovering money from a Zelle scam. Use every option available to you, in the right order.

Bank Dispute

This is always the first step. Contact your bank's fraud department immediately, submit a written dispute, and provide as much documentation as you can. Your chances are highest when you act fast and have clear evidence of deception or unauthorized access.

Fraud Investigation

Once you file a dispute, your bank is required to investigate. Under Regulation E, if your account was accessed without authorization, the bank must reimburse you. If you were deceived into sending money yourself, the legal obligation is less clear, but industry guidelines have shifted toward reimbursement for impersonation scams.

Chargeback Request

Zelle transfers are not credit card transactions, so a traditional chargeback does not apply. But some banks use similar internal processes to reverse peer-to-peer payments. Ask your fraud department specifically whether this option is available for your situation.

Regulatory Complaint

If your bank denies your dispute, a CFPB complaint is your strongest next move. Banks take these seriously because they are required to respond, and patterns of denying legitimate fraud claims attract regulatory scrutiny.

Recovery Method

Success Likelihood

Immediate bank report with documentation

Highest

Police report filed alongside dispute

Raises chances

CFPB or FTC regulatory complaint

Medium, effective for escalation

Late report filed weeks after the scam

Lower, but still worth doing

What to Do After a Zelle Scam

Even after you have reported the fraud and submitted your dispute, stay active. The scam may not be fully over.

Step

Action

Monitor your account daily

Watch for any new unauthorized transactions or access attempts

Change your passwords immediately

Secure your bank account, email, and any linked apps

Set up transaction alerts

Get notified instantly of any future transfers

Freeze your credit

Prevents scammers from opening new accounts in your name

Review linked accounts

Check whether the scammer had access to anything else

If your personal information was exposed during the scam, consider placing a fraud alert with the three major credit bureaus: Equifax, Experian, and TransUnion. This adds a layer of protection while your dispute is active.

Report Fast, Document Everything, and Do Not Accept the First No

Reporting a Zelle scam quickly gives you the best possible shot at recovery. The difference between a case that gets resolved and one that goes nowhere is almost always documentation and persistence.

File with your bank. File with Zelle. File a police report. If your bank denies you, file with the CFPB. At every step, have your evidence organized and ready to submit.

No service can guarantee you will get your money back. But victims who report immediately, document thoroughly, and escalate when necessary recover more often than those who wait.

Sometimes. If your account was accessed without your authorization, reversal is more likely. If you sent the payment yourself after being deceived, it depends on your bank's fraud policy and how quickly you report.

Does Zelle refund scams?

Zelle itself does not issue refunds. Your bank handles the dispute and any reimbursement. Under updated industry guidelines, many banks now reimburse victims of impersonation scams, but outcomes vary by institution and case.

How do I dispute a Zelle transaction?

Call your bank's fraud department immediately. Follow up with a written dispute and attach all supporting evidence: screenshots, messages, emails, and a timeline. Request a case number and check in regularly.

How long does a Zelle investigation take?

Initial review takes 5 to 10 business days. Full investigation can run 10 to 30 days. Final resolution typically comes within 30 to 90 days, though complex cases can take longer.

My bank refused the Zelle refund. What do I do next?

Request a written denial from your bank. Then file a complaint with the CFPB at consumerfinance.gov. File a police report if you have not already. Consider contacting your state attorney general if your bank remains unresponsive.

Can police help with a Zelle scam?

Yes. Police cannot force a reversal, but a police report creates official documentation with a case number that strengthens your bank dispute and supports any regulatory complaints you file.

Being scammed is disorienting, and it can happen to anyone, including careful, smart people who do everything right most of the time. If your stomach just dropped, take that as your cue to act, not to freeze.

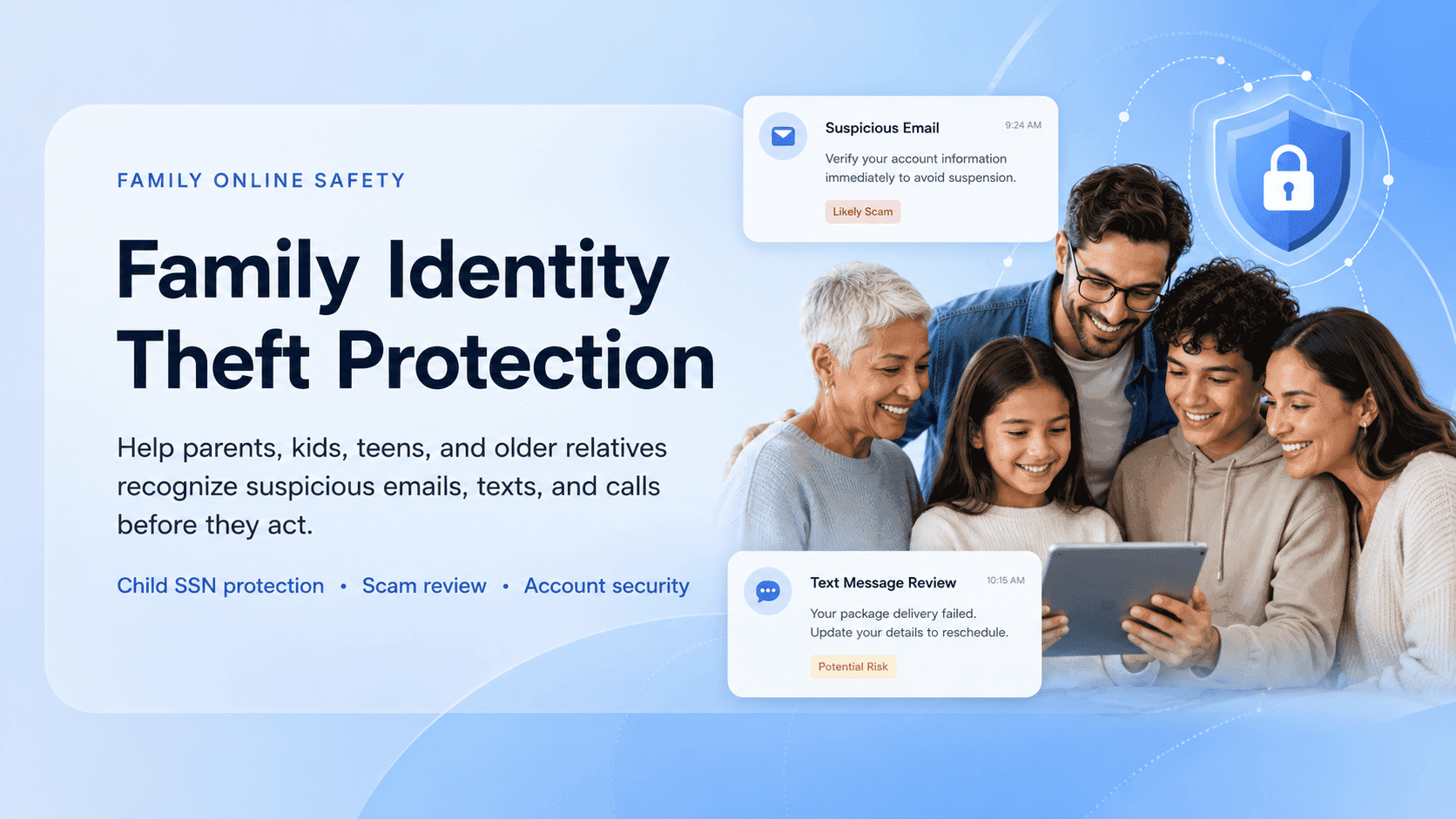

Family identity theft is not just one person's credit card being stolen. In a single household you might have children with unused Social Security numbers, elderly parents targeted by phone scams, adults exposed in data breaches, and shared devices or accounts that create extra risk. Each person faces a different threat, and protecting the family means covering all of them.

Share:

Share: