You lost money to a scam. Then a message arrives promising to get it all back. It feels like a lifeline. Here is the hard part, said gently: the people who reach out promising to undo your loss are often running the second scam.

Share:

That second hit lands harder than the first, because by now you are desperate, and desperation is exactly what they count on.

This guide walks you through how to spot fake scam recovery services, why you keep getting contacted, and what real help truly looks like. You will leave with safe, mostly free next steps, not false hope.

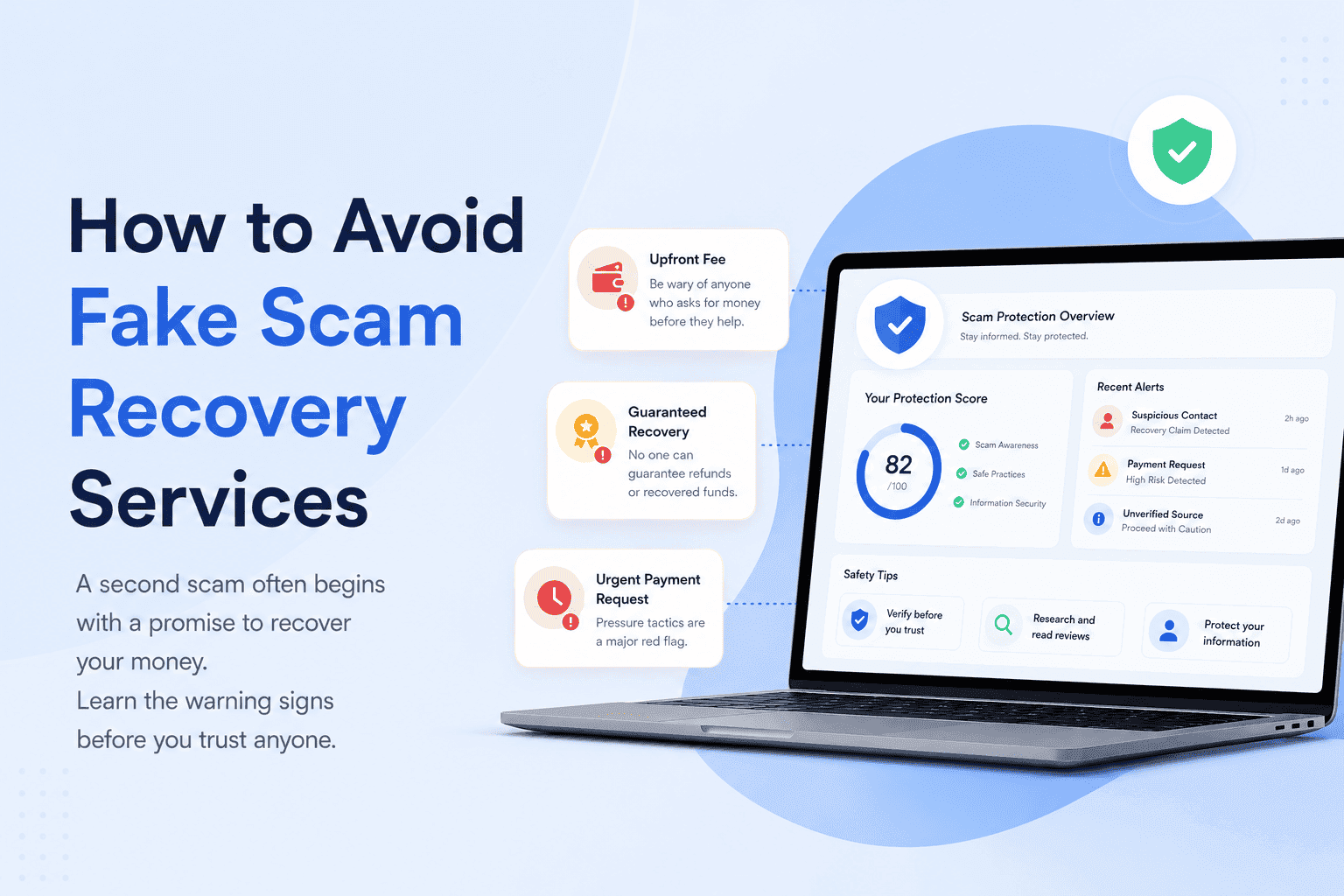

Quick answer: The single biggest red flag is being asked to pay an upfront fee, “tax,” or “retainer” to release your recovered money. Legitimate help, like your bank, the FTC, or the FBI’s IC3, never charges a fee to recover scammed funds and never contacts you out of the blue offering to.

What a “scam recovery service” really means

Scam recovery services cover two very different things, so let’s separate them.

On one side are legitimate channels: your bank’s dispute process, government reporting tools, and a small number of vetted firms that help with chargeback support, documentation, or blockchain tracing for large losses.

On the other side is a much larger pool of “recovery” outfits that exist only to scam victims a second time. Most unsolicited recovery offers, especially ones asking for a fee, tax, retainer, crypto payment, or your personal financial information, are scams.

Here is the honest part. Some money is genuinely recoverable through the right channels, like card disputes, bank recalls, and prompt reporting. But no honest service can guarantee it, and the free official routes always come first.

Why scammers target people who’ve already been scammed

After the first scam, your details do not disappear. Your name, contact info, the amount you lost, and the type of scam often get reused or sold. The FTC calls these “sucker lists,” and they are exactly why prior victims get hit again, sometimes more than once.

Sometimes it is a fresh crew working from a purchased list. Sometimes it is the original scammer coming back months later, now wearing a “recovery agent” hat.

The emotional truth matters here. You want the loss undone. That pull is normal, and it is the precise feeling a recovery scam is built to exploit. Naming it out loud helps you stay skeptical when the “good news” call comes.

First, an unsolicited contact. A call, email, or DM from a “government official,” “attorney,” or “recovery agent.” Then the hook: your money has been found, a court is distributing funds, or the scammer has been caught. There is just one small thing in the way, a “donation,” a retainer, an overdue tax. You pay it. Then another fee appears. Then another. Nothing ever comes back.

To sell it, they lean on credibility props. Fake press releases dressed up as news. References to real agency advisories. Spoofed agency names and lookalike websites. The FBI has even warned that scammers now impersonate IC3 itself, the very place you would go to report.

Picture how it feels from the inside. The caller knows the exact amount you lost. They know the platform. They might even know the scammer’s fake name. To you, that looks like proof they are the real deal. In reality, all of it came from the sucker list, and they are reading it back to you to lower your guard. The more they “know,” the more you should slow down, not speed up.

A second tactic worth knowing: layered fees. The first ask is small and reasonable-sounding, maybe a “processing fee” or a “small tax.” Once you pay, the story shifts. Now there is a customs hold, a legal filing cost, a bank verification charge. Each one feels like the last hurdle before your money lands. There is no last hurdle. The fees stop only when you do.

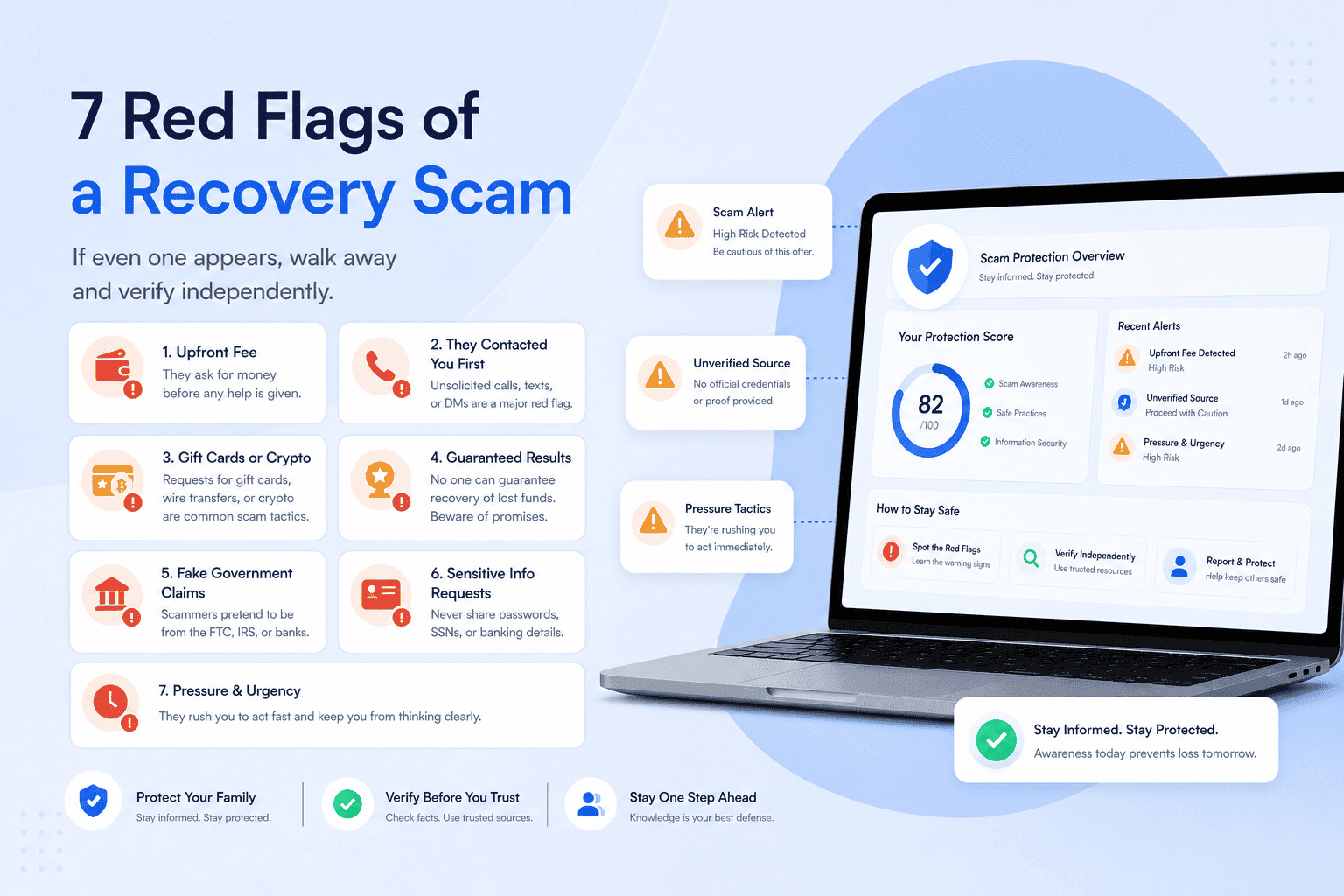

The red flags: how to spot a fake recovery service

Run any offer through this list. These are the red flags that separate fake scam recovery services from genuine help, and one match is enough to walk away.

They ask for money up front

Any “fee,” “tax,” “retainer,” “donation,” or “bond” to release your funds. This is the number one tell. The logic they use sounds plausible at first: “We just need to cover the transfer cost,” or “There’s a small tax before the funds clear.” But real recovery never works that way. Money owed to you is not held hostage behind a payment you have to make. If you have to pay to get paid, it is a scam.

They contacted you first

An unsolicited call, email, DM, or social message offering recovery. Real agencies do not cold-contact victims with recovery offers. They have no way of knowing you were scammed unless you reported it to them directly, or unless your details are already circulating on a sucker list. An out-of-the-blue “we can get your money back” message is the opening line of the second scam, not a coincidence.

They demand unusual payment

Wire transfer, gift cards, prepaid cards, crypto, or a payment app. All hard to reverse, all favorites of scammers. Notice the pattern: every method they push is one where the money disappears the moment you send it. A legitimate firm working with you on a real claim does not ask for gift cards. No court, bank, or agency on earth collects a fee in iTunes codes.

They guarantee results

“We will get 100% of your money back.” No honest service guarantees recovery, because recovery depends on factors nobody controls, like how the money moved, how fast you acted, and whether it can be traced. A guarantee is not confidence. It is bait, and it is designed to make you stop comparing them against the free official routes.

They claim to be the government, or to already have your money

Real regulators never call offering paid recovery, and never say funds are recovered but you must pay to get them. If someone claims to be from the FTC, FBI, or a “federal recovery task force,” hang up and call the agency yourself using a number from its official website. Agencies that genuinely handle restitution notify eligible victims by mail, not by surprise phone call.

They want sensitive info first

Banking details, ID, photos, or logins before they show you any fees or service terms. Never hand these over. A common trick is to ask for “verification” documents that are really just the next round of identity theft. The order is backwards on purpose: a real provider explains its service and costs before asking for anything sensitive.

They push urgency and email links

“Act now or lose the window.” Urgency is the scammer’s favorite tool because it stops you from thinking and checking. Don’t click links in recovery emails. Look up the organization yourself and contact it directly. A genuine offer survives a day of you doing homework. A scam does not, which is why they cannot let you wait.

Here is how these flags stack up in real life: Someone calls, warm and reassuring, says your $4,000 loss has been “located in a recovered asset pool,” and that a $250 release fee is all that stands between you and your refund. They knew the amount. They sounded official. They wanted it wired today. Four red flags in one call: an upfront fee, an unsolicited contact, a wire demand, and manufactured urgency. That is not a near-miss with a real recovery service. That is a textbook second scam, and the right move is to hang up and report it.

Crypto recovery services: a special warning

This is the highest-risk category by far, and it draws the most fake-recovery activity.

The cons are predictable. “No upfront cost” crypto recovery firms that later demand a “gas fee” or “tax.” Bogus blockchain-tracing dashboards that show impressive-looking progress. Outfits that ask to be paid in more crypto.

Here is the reality check, kept honest: most crypto sent to a scammer is not recoverable. The legitimate first steps are reporting to the exchange, to the FTC, and to the FBI’s IC3 cryptocurrency unit, not paying a “recovery expert.” If you are weighing crypto reporting tools, our breakdown of crypto scam reporting lays out what each one does.

What legitimate help really looks like

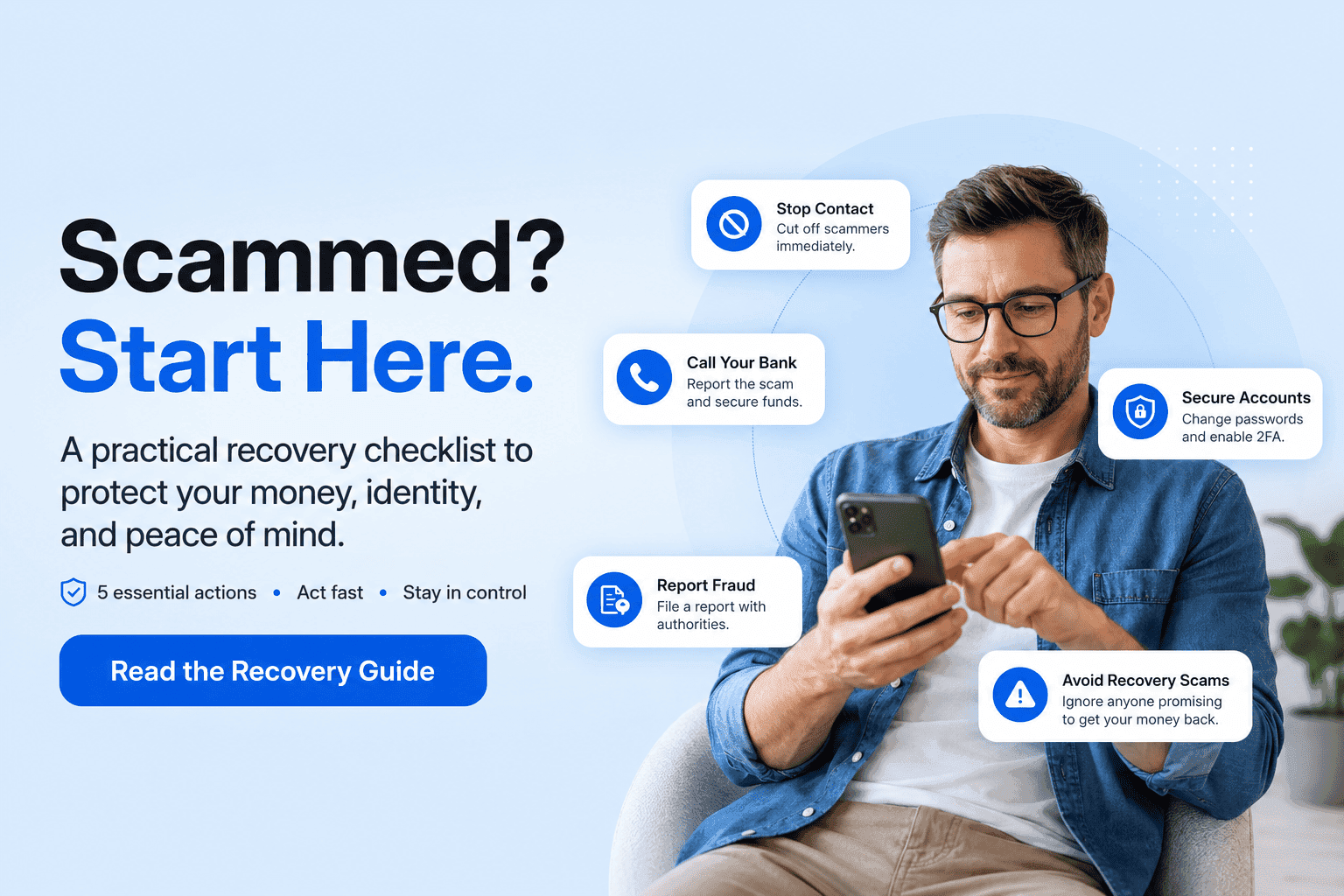

You are not out of options. The real routes are mostly free, and they start with steps you can take today.

Dispute the charge with your bank or card issuer. Ask your bank to recall a wire if it is recent. Report the scam to ReportFraud.ftc.gov and, for online or crypto cases, to the FBI’s IC3 complaint form. And protect your identity with a fraud alert or credit freeze.

Timing matters more than most people realize. Card disputes and wire recalls work best when you move within days, not weeks, so the order of operations is simple: contact your bank first, report second, lock down your credit third. If a payment app like Zelle was involved, the steps and timelines are specific, and our walkthrough on how to report a Zelle scam covers what to ask your bank and when to escalate.

One important clarification on these reports: FTC and IC3 reports create official records and help law enforcement spot patterns. They are not paid recovery services, and they do not guarantee individual refunds. The FTC shares reports with law enforcement but cannot resolve individual cases. The value is real, but it is about evidence and pattern-spotting, not a check in the mail.

On protecting your credit, know the difference. A fraud alert can be placed by contacting just one credit bureau, which must notify the other two. A credit freeze is stronger but requires contacting all three bureaus separately. If you are sorting out which protection you need, this guide on identity fraud vs identity theft is worth a read.

When can a paid service be legitimate? In narrow cases, for large or complex losses, a paid provider may help with documentation, legal claims, chargeback support, or blockchain tracing. But no legitimate provider should guarantee recovery, demand a “release fee,” ask for crypto or gift-card payment, claim an official government partnership, or pressure you. Verify it independently before you trust it.

Unscammed will never ask you to pay a fee, tax, or retainer to release recovered money. We help you report the scam to the right agencies and protect your identity, the legitimate way.

Already been contacted by a recovery scammer? Do this

Stop and breathe. Then act.

Don’t pay. Don’t click. Don’t share more information. Stop responding to them.

Verify independently. Look up the agency or firm yourself and contact it through its official site, never the numbers or links they gave you.

Report the follow-on attempt to the FTC and IC3, and place a fraud alert on your credit so one bureau notifies the other two. If your identity was exposed, filing an identity theft police report creates a paper trail that helps later.

How to vet a recovery company before you trust anyone

A few minutes of checking saves you from the second loss. The same steps work whether you are vetting a single firm or comparing several scam recovery services.

Verify the company is registered with the relevant regulator. Confirm a real physical address and a genuine track record. Get every fee and term in writing. Apply the no-upfront-fee rule without exception. Then search the company name alongside “scam” and “reviews,” and check regulator and BBB complaints. If something is wrong, it usually surfaces fast.

For a wider view of where to report different fraud types, our roundup of top scam reporting platforms covers identity theft, crypto, and payment scams in one place.

Frequently asked questions

Are scam recovery services legit?

A few legitimate firms and free official channels exist, but most unsolicited recovery offers are scams. The clearest test: if they ask for an upfront fee, “tax,” or “retainer” to release your money, walk away.

Should I ever pay a fee upfront to recover scammed money?

No. Legitimate agencies never charge an upfront fee to recover funds, and demanding one is the single biggest red flag of a recovery scam. Report anyone who asks.

Why do recovery companies keep contacting me after I was scammed?

Your information often ends up on a “sucker list” that scammers reuse or sell, so prior victims get targeted again, sometimes by the original scammer. Being contacted is itself a warning sign, not a lucky break.

Are crypto recovery services real?

Most unsolicited ones are not. Be especially wary of “no upfront cost” firms that later demand a “gas fee” or payment in more crypto. Most crypto sent to a scammer cannot be recovered, so report it to the exchange, the FTC, and IC3 instead.

A recovery company says they already have my money. Is that true?

Almost certainly not. A common script claims the money is recovered but you must pay a fee or tax to release it. Real agencies do not work that way and notify eligible victims of restitution by mail.

What does legitimate scam recovery help look like?

Mostly free, official routes: dispute the charge with your bank, ask your bank to recall a wire, and report to ReportFraud.ftc.gov and ic3.gov. Any paid firm should be transparent about fees in writing, never guarantee results, and never pressure you.

How do I report a fake recovery service?

Report it to the FTC at ReportFraud.ftc.gov and, for online or crypto cases, to the FBI’s IC3 at ic3.gov. Don’t click links they sent. Look up agencies independently.

How can I vet a recovery company before trusting them?

Verify it is registered with the relevant regulator, confirm a real address and track record, get all fees in writing, apply the no-upfront-fee rule, and search the company name alongside “scam” and “reviews.”

Don’t get scammed twice

The first loss was not your fault. You were targeted. The second loss is the one you can stop right now, just by recognizing the pattern: real help does not cold-call you, does not guarantee results, and never asks you to pay to get your own money back.

If a “recovery” offer is making you uneasy, trust that feeling. Most fake scam recovery services give themselves away within the first few minutes if you slow down and check. Take the free, official steps first. And if you are not sure where to start, what to do after being scammed is a solid starting point from the FTC.

Worried a “recovery” offer might be a second scam? You don’t have to figure it out alone. Unscammed helps you take the real, safe next steps after fraud.

Being scammed is disorienting, and it can happen to anyone, including careful, smart people who do everything right most of the time. If your stomach just dropped, take that as your cue to act, not to freeze.

Family identity theft is not just one person's credit card being stolen. In a single household you might have children with unused Social Security numbers, elderly parents targeted by phone scams, adults exposed in data breaches, and shared devices or accounts that create extra risk. Each person faces a different threat, and protecting the family means covering all of them.

Share:

Share: